October’s Macedonian PGM imports have been released. To recap, this is my go-to data on whether substitution of platinum for palladium is taking place in diesel catalysts (for more details see embedded post below) as Macedonia imports PGMs for only one reason – to go in diesel catalysts.

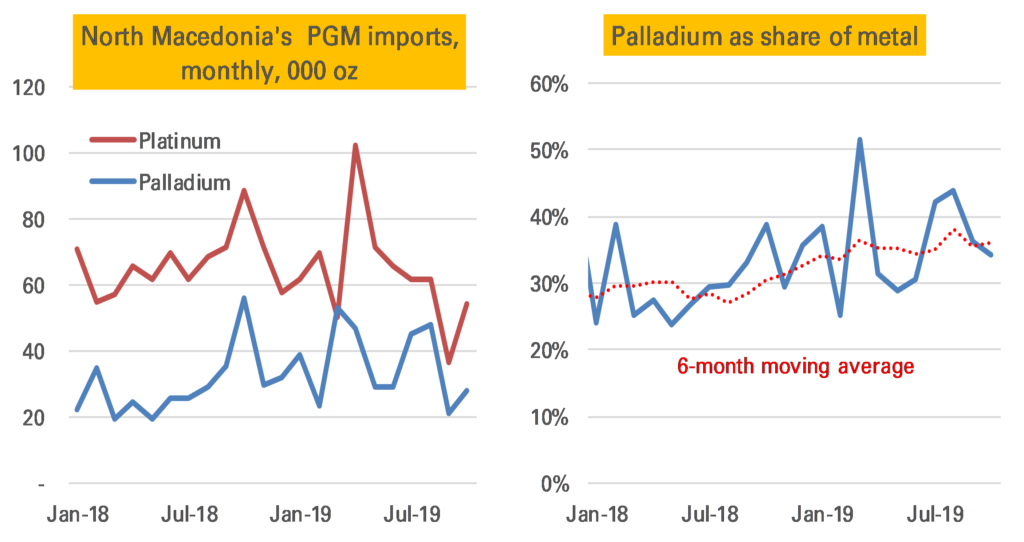

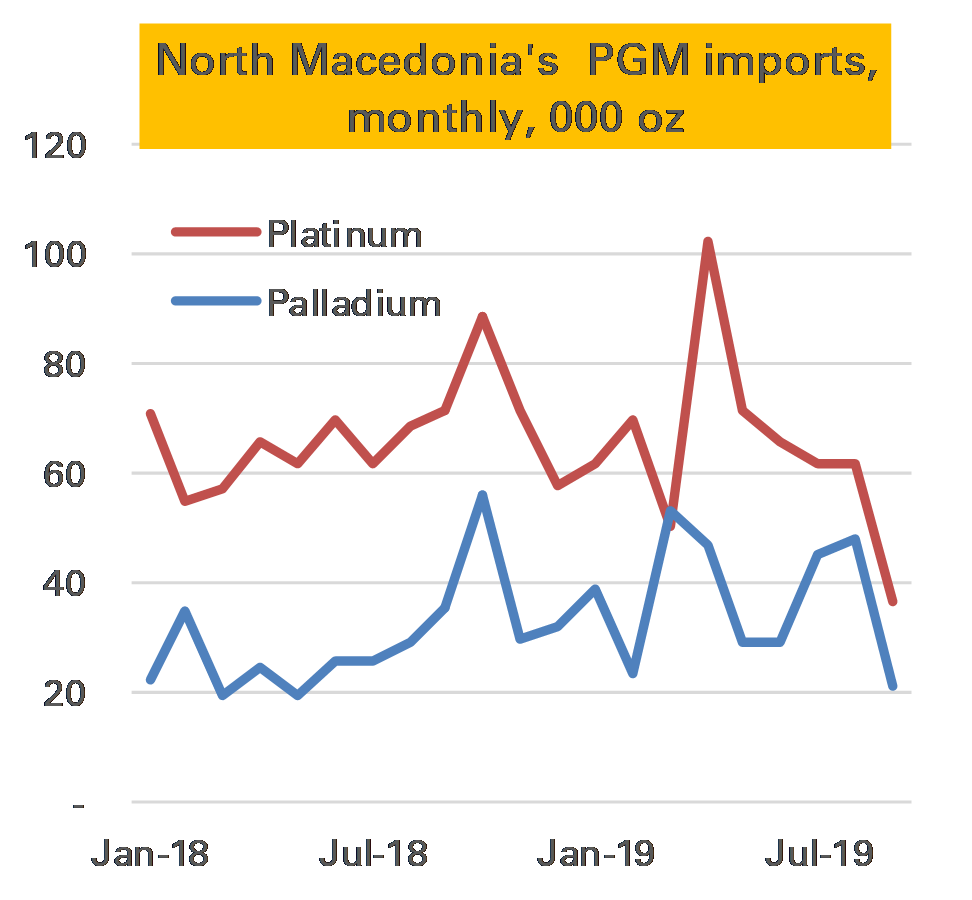

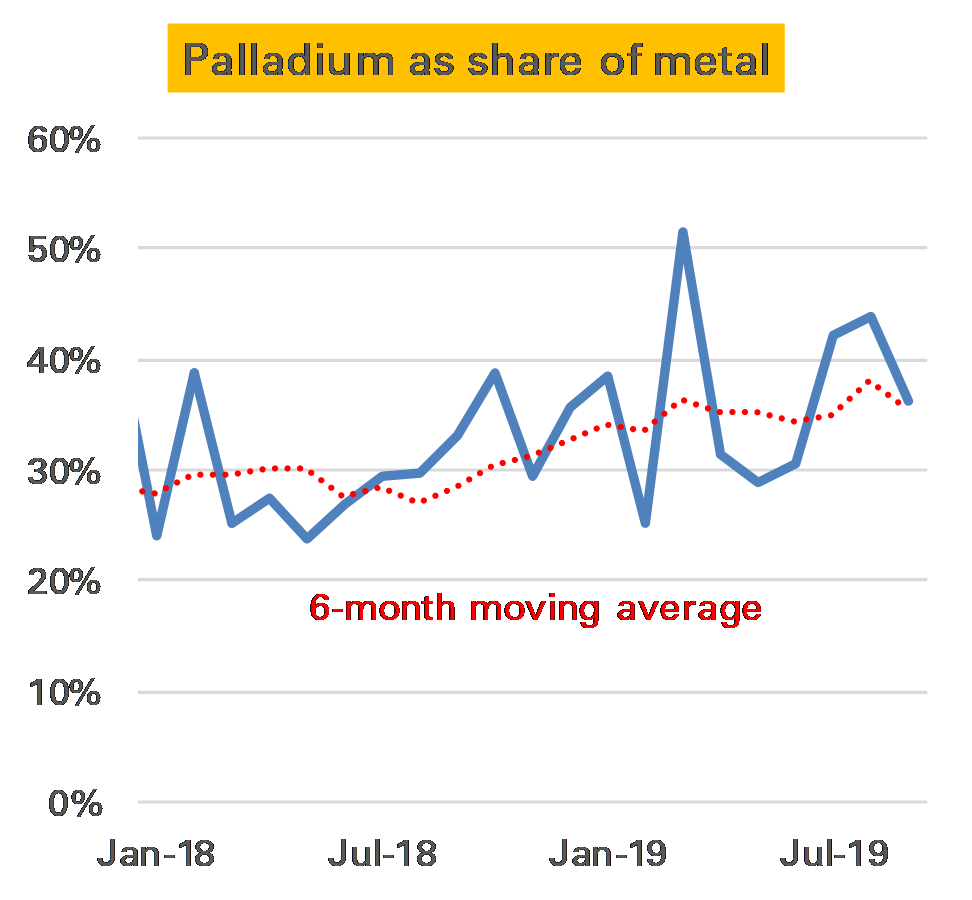

It was not a particularly exciting month. Both platinum and palladium imports picked up from a weak September, and the ratio of palladium was slightly lower than the recent average at 34%. Nevertheless as the second chart below show it would be a stretch to see this as any kind of price-related substitution.

There’s no doubt, by the way, that palladium is costing a lot. The import price of that metal averaged $1700/oz, a new record, and far more than the platinum cost of $890/oz. As such the dollar cost of the two metals’ import was much the same, despite the much larger volume of platinum.

For more details on this measure see these two previous posts.

September’s Macedonian trade data is out, important for PGM market participants as it is the best way I can come up with to track whether super-expensive palladium is being substituted out of the diesel catalysts for cheaper platinum 1.

So far there has been no evidence of such substitution, indeed the palladium ratio of the two metals has actually trended higher through most of this year.

September was a little different. Imports of both metals plunged, but because palladium fell more sharply, the implied ratio did move in platinum’s favour, to 36% by weight, compared to 44% in August’s data.

Source: UN comtrade, Matthew Turner, November 2019

But it’s way too soon to read anything into this. 36% is actually the six-month average, and higher than seen in many months this year.

The sharp fall in imports of both metals is quite interesting. It seems unlikely there is going to be sharp fall in output so one suggestion that comes to mind is metal was being stockpiled ahead of potentially disruptive “no-deal” Brexit (the metal comes from the UK), though that is guesswork.

What is clear is the imported price of palladium is rising fast. In September it was $1,570/oz, the highest on record. That corresponds to the market price in the first part of the month – October’s was much higher.

Notes:

For details of why this is the case, which in short because Macedonia’s main importer is a huge JM catalyst factory, see here↩

Answer: it wasn’t and that was a good reason to think the price of palladium could go higher. And indeed it has gone higher, now nearing $1,800/oz.

We now have North Macedonia trade data for August. Does this show any shift towards platinum? Nope. Palladium was 44% of the palladium & platinum imported, higher than the YTD average of 36%. This reinforces the point that 2019 is on course to see palladium’s share rise not fall.

In today’s latest World Economic Outlook (WEO) the IMF devotes a large-ish section to gold and other precious metals (p.47 onwards here).

Perhaps the most interesting section is on whether they serve as an inflation hedge. Finding a positive but weak correlation to inflation itself, the analysts also look at gold prices against modelled inflation risks. Here they are more positive, saying:

Results of the analysis support the view that precious metal prices react to inflation concerns… An increase in inflation uncertainty by one standard deviation tends, within a month, to raise the price of gold by 0.8 percent and silver by 1.6 percent. A decline in inflation uncertainty can explain half of the observed gold price decline of the 1990s and one-third of the price rise after 2008. The role of inflation uncertainty is, instead, positive but not significant for platinum and palladium, yet irrelevant for copper

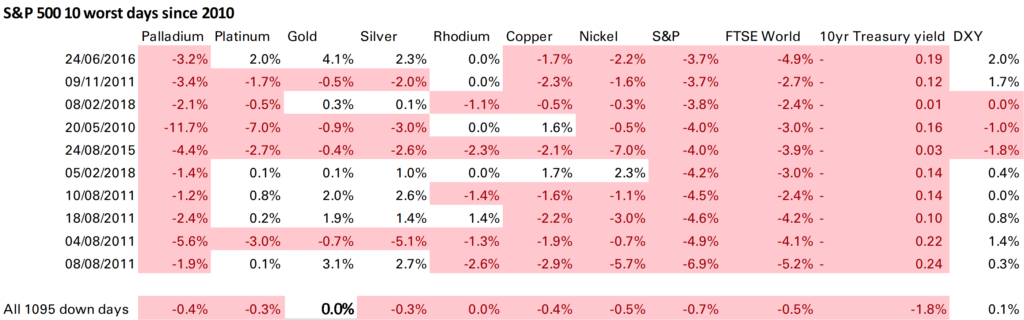

For many gold’s main advantage is not inflation but against systemic risk. The IMF also looks at this through reactions to S&P 500 moves. This is something I have long done, and the IMF’s conclusions are the same – gold does act as a safe haven when the S&P 500 falls, silver does but less so, and the other metals do not. Here’s one of my versions of this table.

Finally the IMF also mentions precious metals’ sensitivity to dollar moves. But only to express surprise the beta can sometimes be more than 1 (ie if the dollar falls 1%, gold rises more than 1%). I think this relationship – which is partly obvious given we are quoting the price in dollars – needs more discussion and will do so in a later post.

The palladium price has hit a new record high in recent days over $1,700/oz, and the FT has declared there’s more to come unless we see a global recession or substitution of much cheaper platinum. I agree. And yet at present not only is there no evidence of substitution but there’s evidence that there has been no substitution.

It comes from North Macedonia.

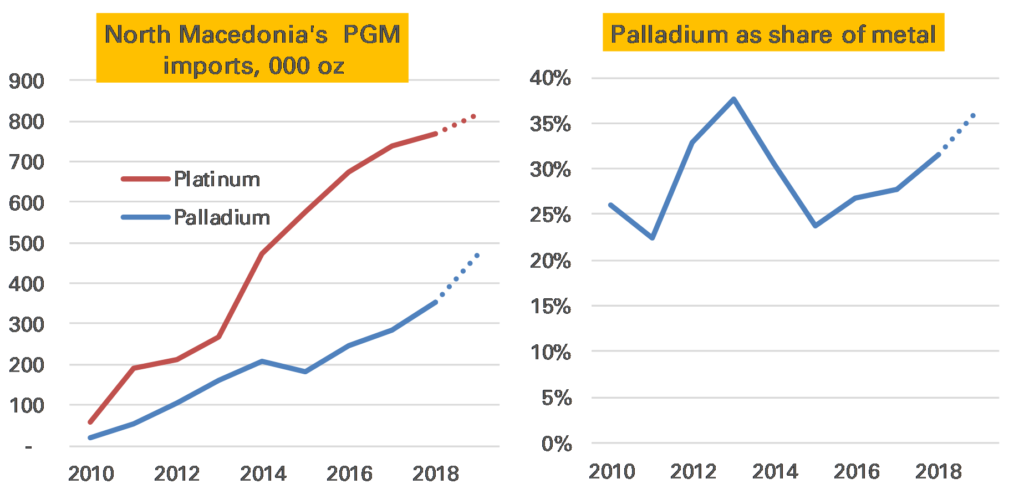

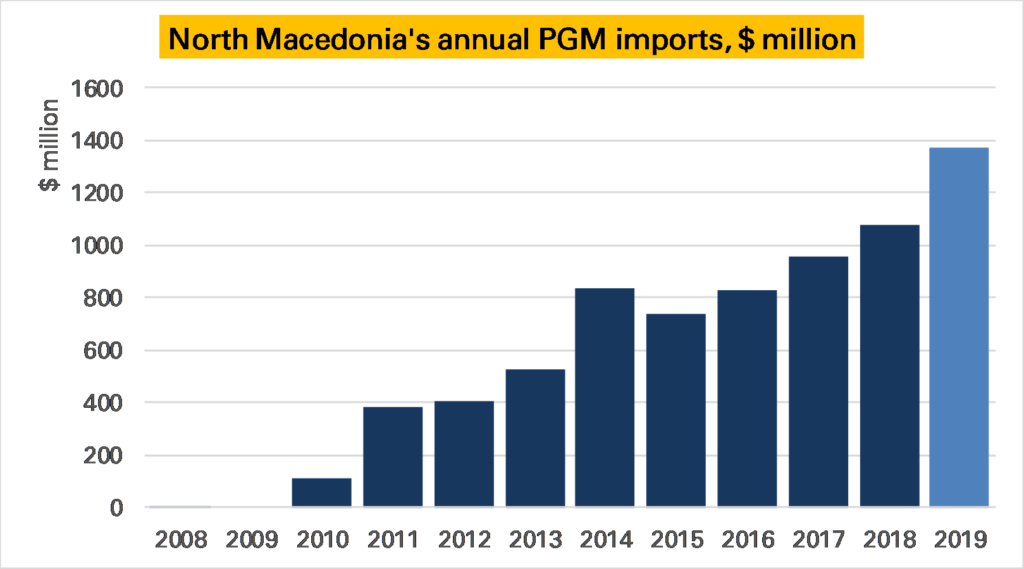

This country had little to do with the global PGM markets for much of its history. It is not a producer, and in 2009 reported imports of unwrought PGMs of only $1. That might sound a little implausible, but probably not far from correct – in 2008 PGM imports were less than $20,000.

And yet in 2010 it imported over $100m of PGMs. And by 2018 this was over $1bn, with more than 1 Moz of PGMs imported. This year is approaching $1.5bn.

Source: UN comtrade, Matthew Turner. Note 2019 extrapolated from first 7 months of the year.

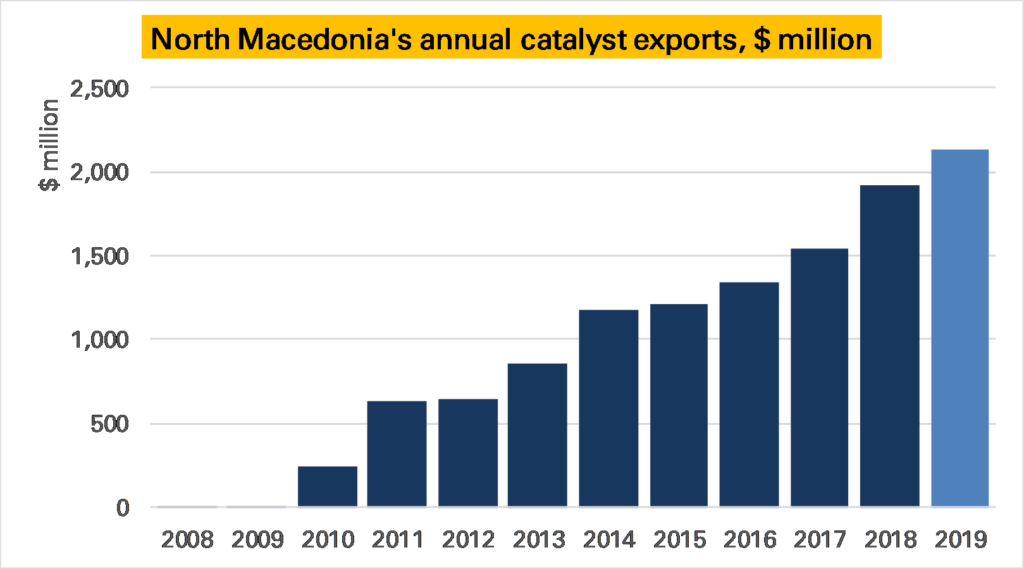

What gives? In 2010 refiner Johnson Matthey (JM) opened a diesel autocatalyst plant, which was expanded in 2013. This is why North Macedonia’s exports of catalysts also exploded, rising from nothing in 2008/2009 to nearly $2bn in 2018 (Macedonia has not gone its own car industry).

Source: UN comtrade, Matthew Turner. Note 2019 extrapolated from first 7 months of the year.

This is great for an analyst. Other large catalyst manufacturing countries are also PGM traders, such as the UK, and/or jewellery consumers, such as the China and the USA. This means it is hard to draw firm conclusions from trade data. But in North Macedonia it is just catalysts – therefore it is safe to assume the imported PGMs are being used in that sector.

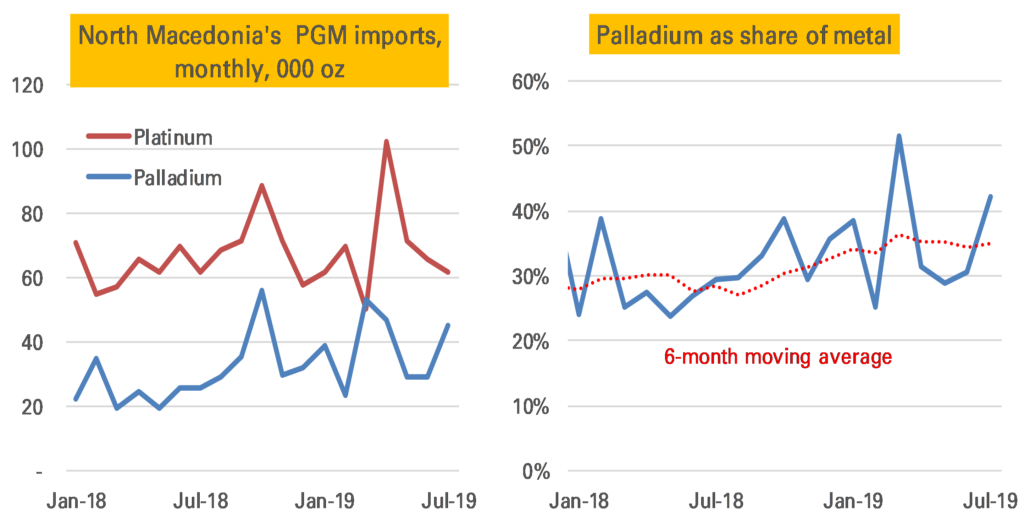

As such because we can break the trade data out by metal we can use it to estimate what proportions of platinum and palladium JM are putting in their catalysts. If we look at its imports by volume, we see that more platinum is imported than palladium – in 2018 nearly 800 koz of the former to around 350 koz of the latter – making palladium 28% of the combined volume to platinum’s 72%. This is to be expected given the plant is producing diesel catalysts. But importantly this proportion of palladium in the mix doesn’t seem to have fallen in the last few years – indeed it modestly rose from 24% in 2015*.

Source: UN comtrade, Matthew Turner. Note 2019 extrapolated from first 8 months of the year. This chart was corrected on 23-10-2019 as date axis misaligned and so includes August data.

Perhaps the shift has only happened in the last few months? Not that either. Indeed while monthly import data is quite volatile, if there is a clear trend it is the other way, with palladium seeing a share of 50% in one month.

Note: The right-hand chart on 24-10-2019 replaced an earlier one which in error showed palladium relative to platinum, not as a share of all metal.

This data can’t prove no substitution is taking place. There could be other effects masking it, for example if JM have been importing additional palladium than they are using in catalysts (indeed it looks likely), perhaps ahead of the rising price or Brexit. It also might be that the mix of heavy and light vehicle autocatalyst could have changed, affecting the ratio (that’s what seems to have driven palladium’s share down in 2013 after the plant’s first expansion). And if the plant had begun manufacturing gasoline catalysts all bets would be off, though then we would also see rhodium imports, and we have not.

We also can’t assume that JM’s Macedonia plant is representative of all their catalyst plants or those of other catalyst manufacturers. And it is possible substitution is happening in gasoline catalysts, not diesel ones.

Nevertheless it is strong evidence that there has been no substitution. After all most analysts believe if substitution is to come it would come first in diesel, where car and catalyst makers are most comfortable with using platinum.