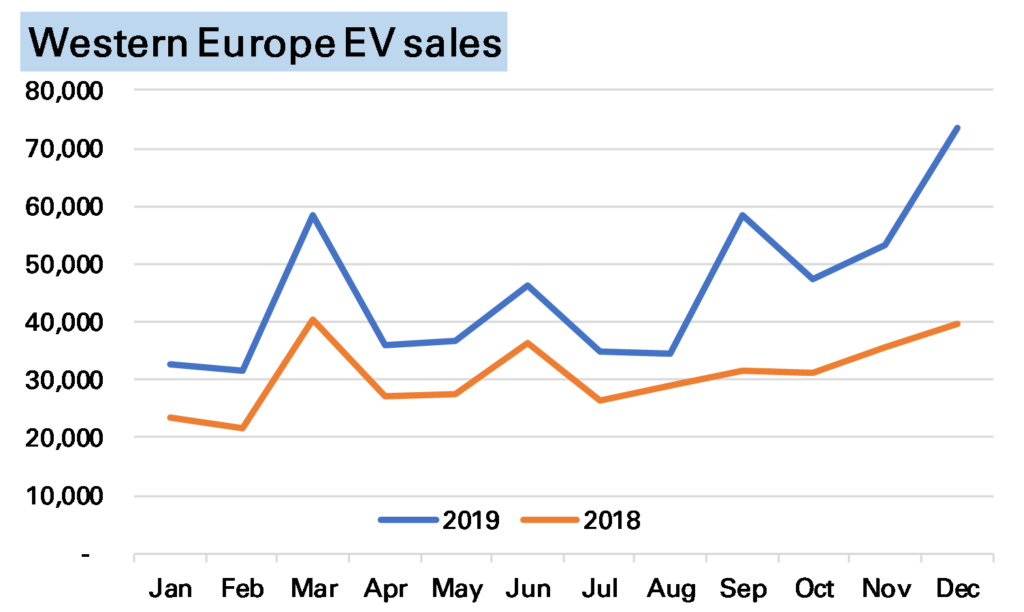

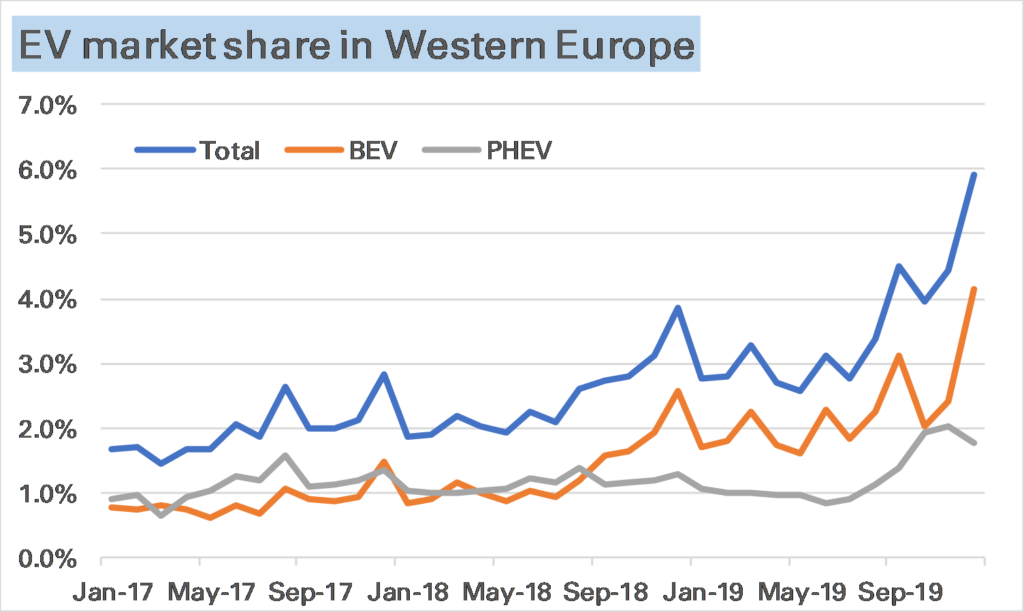

European electric car sales in December set a new record, at an estimated 74k units, a huge 85% higher than in December 2018. Market share, as shown in the 2nd chart, was nearly 6%, primarily made up of pure battery-electric vehicle (BEVs), up 94% YoY, while plug-in hybrids (PHEVs) were up 68% YoY but slightly down on November’s level.

Source (this and other charts): European national car associations.

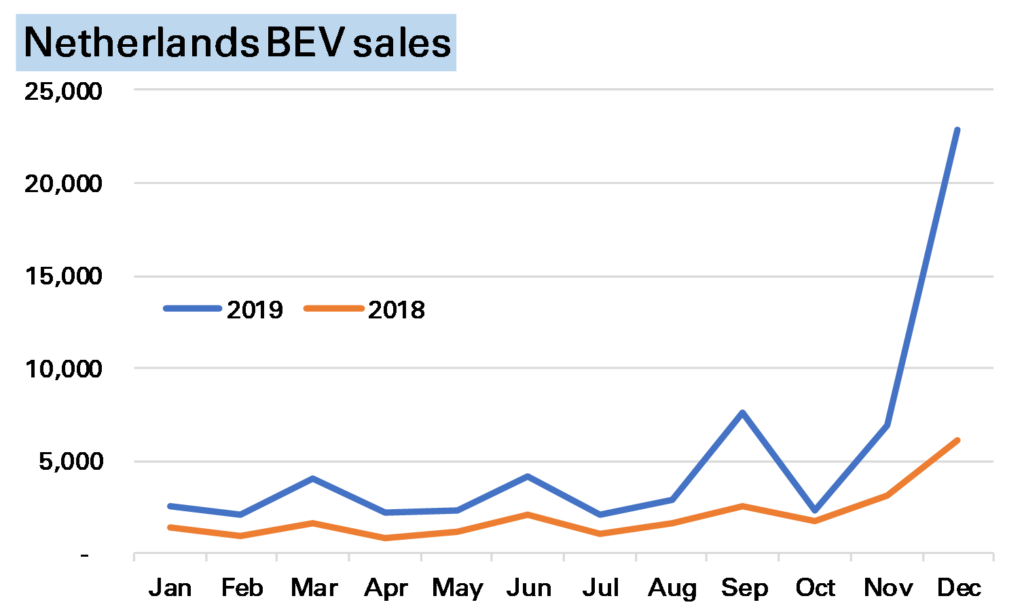

While European EV sales have been strong all year, December’s surge is somewhat misleading as to the underlying strength of the market. End-year can often see odd movements in EV sales as the market remains dominated by subsidies which often expire at that time. The most notable example this month was in the Netherlands, where higher taxes in 2020 brought forward purchases, seeing EVs take more than 50% market share and BEVs on their own sell nearly 25,000 units, a third of the European market.

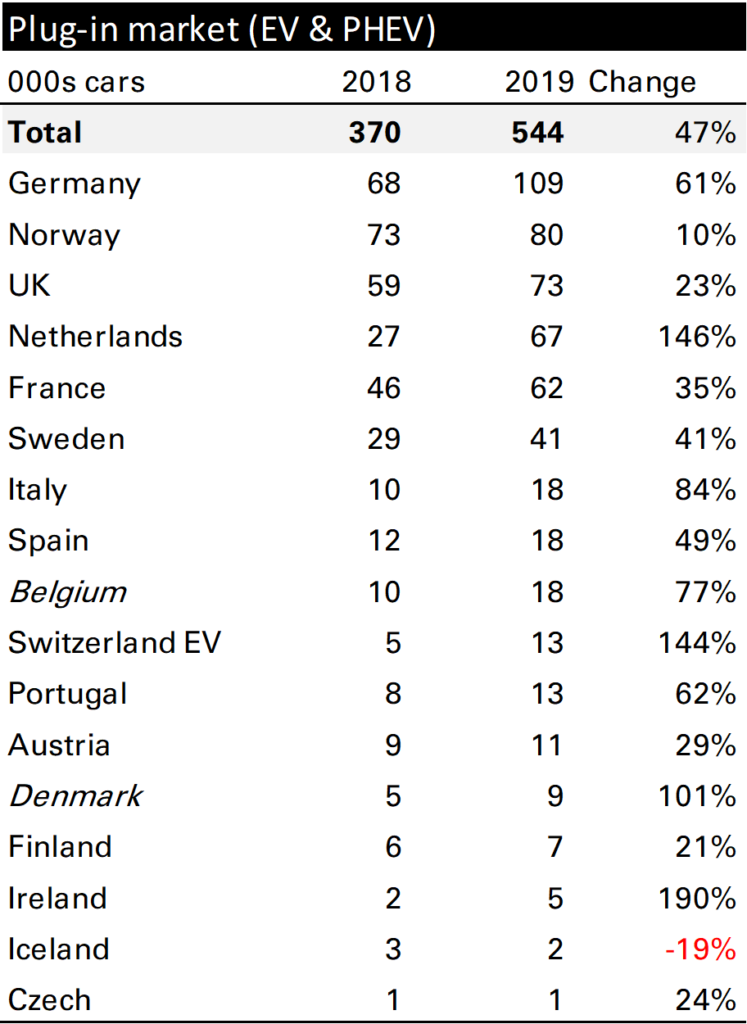

Without the Netherlands European EV sales in December would have been up less than 40%, the level which has been my base case for annual growth for a while. For the year as a whole European EV sales grew 47% (of course helped by that Netherlands surge) to 544k vehicles, a market share of 3.5%, from 370k vehicles, and 2.4% in 2018. Most markets were strong, but of the larger ones Germany stands out, up 61%. It’s also worth noting that BEVs massively outperformed PHEVs, gaining 80% to the latter’s 10%.

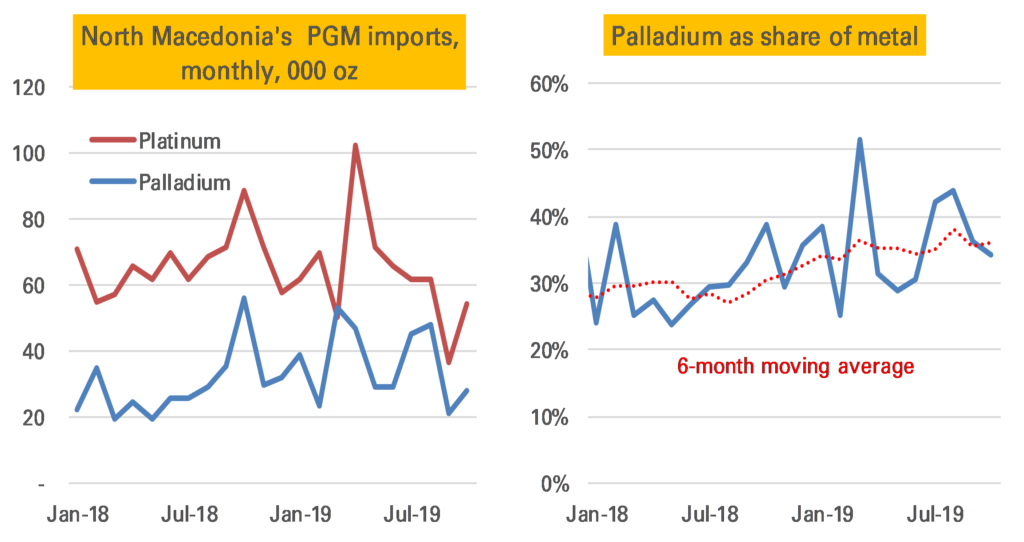

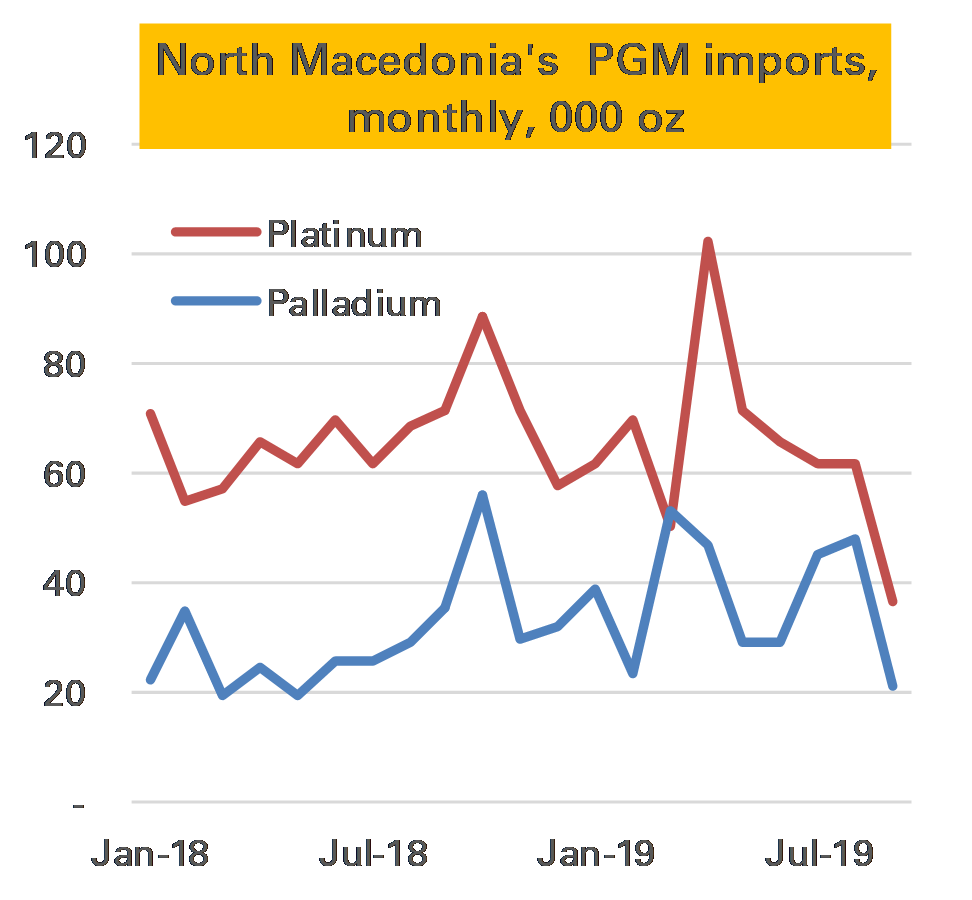

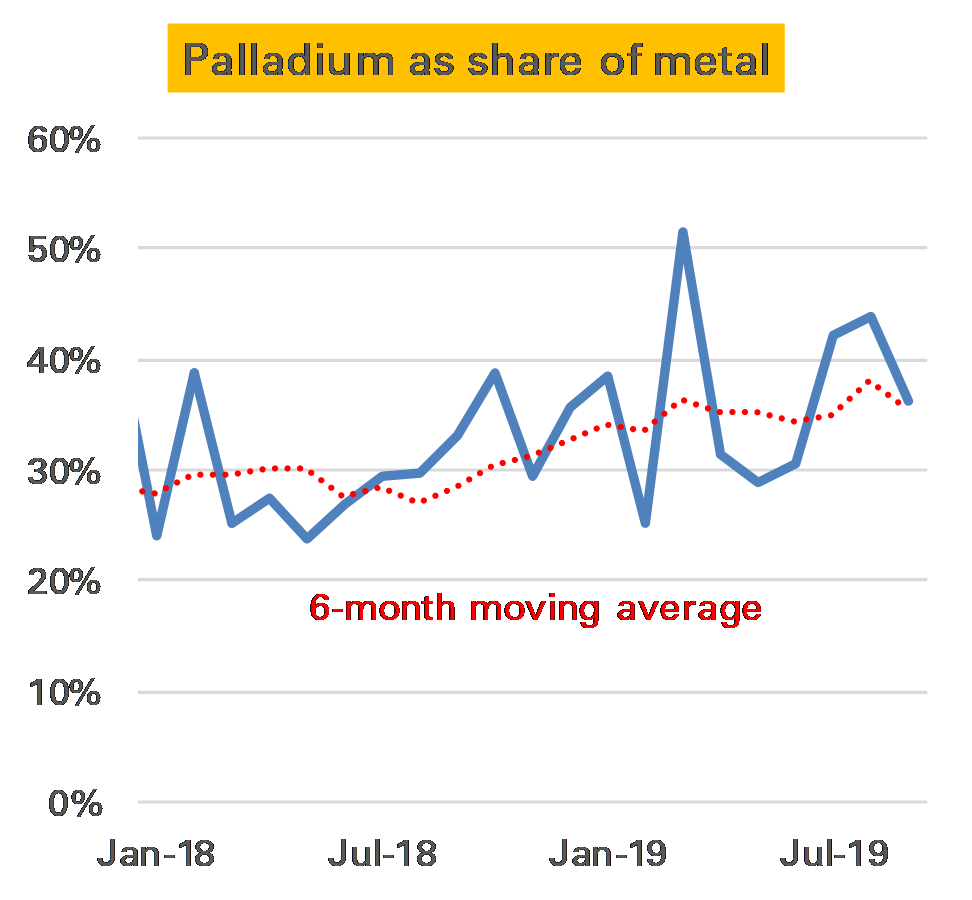

October’s Macedonian PGM imports have been released. To recap, this is my go-to data on whether substitution of platinum for palladium is taking place in diesel catalysts (for more details see embedded post below) as Macedonia imports PGMs for only one reason – to go in diesel catalysts.

It was not a particularly exciting month. Both platinum and palladium imports picked up from a weak September, and the ratio of palladium was slightly lower than the recent average at 34%. Nevertheless as the second chart below show it would be a stretch to see this as any kind of price-related substitution.

There’s no doubt, by the way, that palladium is costing a lot. The import price of that metal averaged $1700/oz, a new record, and far more than the platinum cost of $890/oz. As such the dollar cost of the two metals’ import was much the same, despite the much larger volume of platinum.

For more details on this measure see these two previous posts.

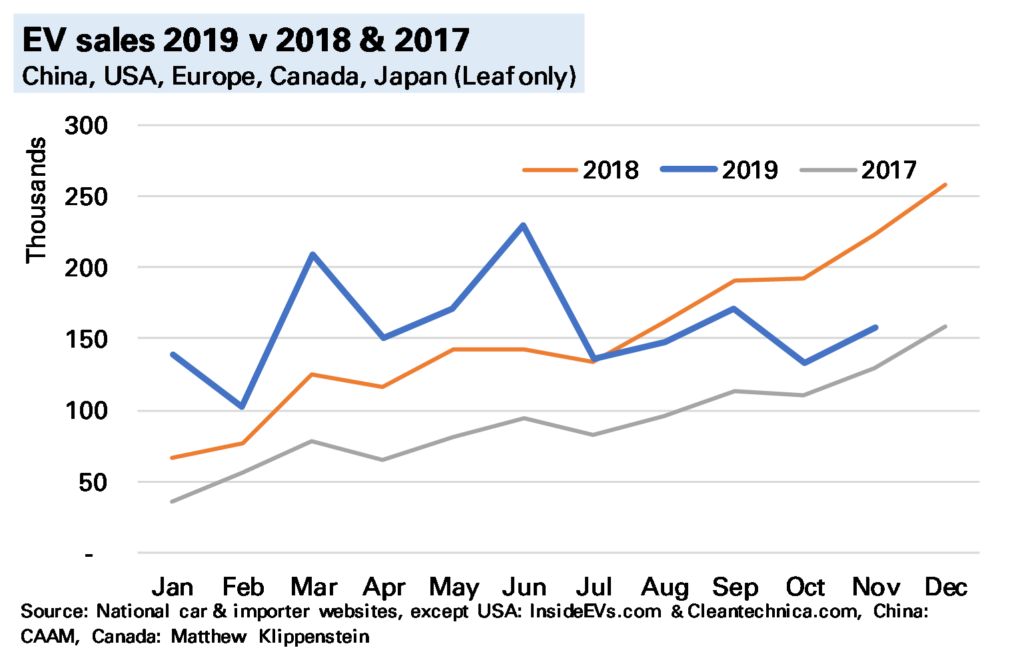

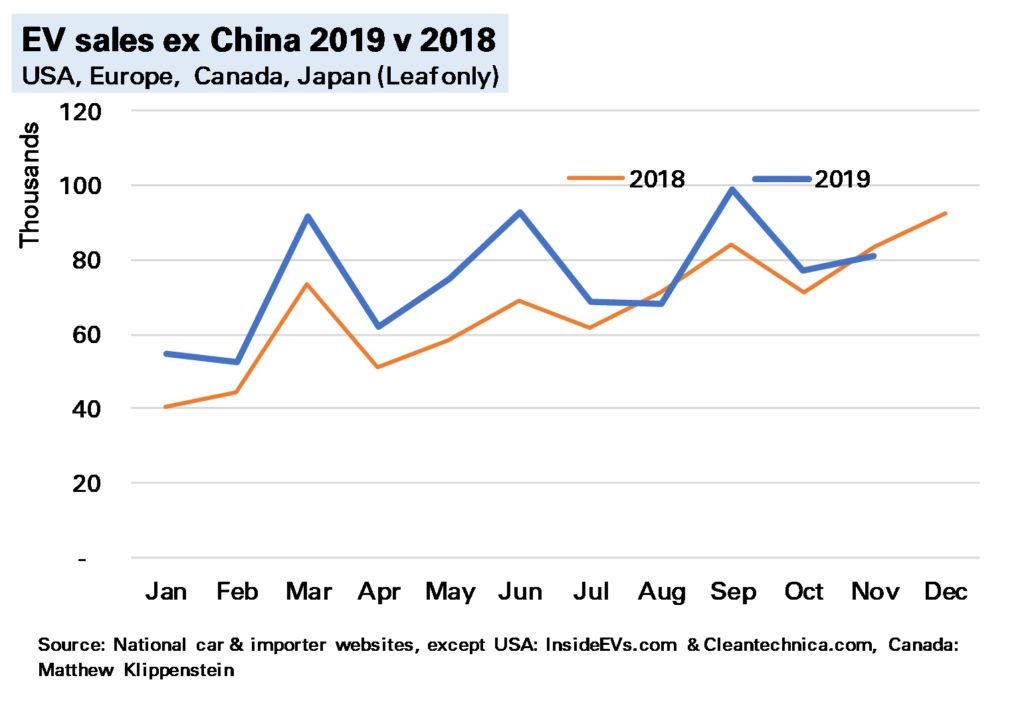

In November global electric vehicle (EV) 1 sales I estimate were about 160k, 29% lower YoY, continuing the slump seen in recent months.

China accounts for most of the slowdown, being by far the largest market and down 45% YoY, little better than in October. Europe, on the other hand, while still a considerably smaller market, posted another solid growth rate of 49% YoY. The difference between the two markets is largely incentives – much lower in China since mid-year but remaining strong in Europe. The USA looks to be running somewhat lower than last year, though we await better data at year-end.

Overall, as the final chart shows, even excluding China, EV sales in November were no higher than in the same month of 2018.

(Note click on charts to show at full size)

With just one month to go it’s clear 2019 has been a disappointing year. Year-end is hard to predict but on current trends global EV sales are likely to be just under 2m, only 6% higher than in 2018. Chinese EV sales are likely to be flat or slightly down, as are US EV sales, while Europe will be up 40-50%. This will mean while China’s share of global EV 2 sales falls from 56% to just over 50%, Europe’s will have risen to 27% from 20%.

Notes:

China, USA, Europe, Japan Nissan Leaf. Exclude Chinese light commercial vehicles – another 10k or so – and perhaps another 10k vehicles in the rest of the world, most notably Korea ↩

Again this excludes the large – 130k or so in 2019 – Chinese commercial EV market ↩

It seems very important but analysts tend to ignore gold’s voluminous above-ground stocks. I’ve always thought this was a mistake, but I’m still not quite sure the best way to approach it. This is an idea I’ve had but it’s still very much a work-in-progress.

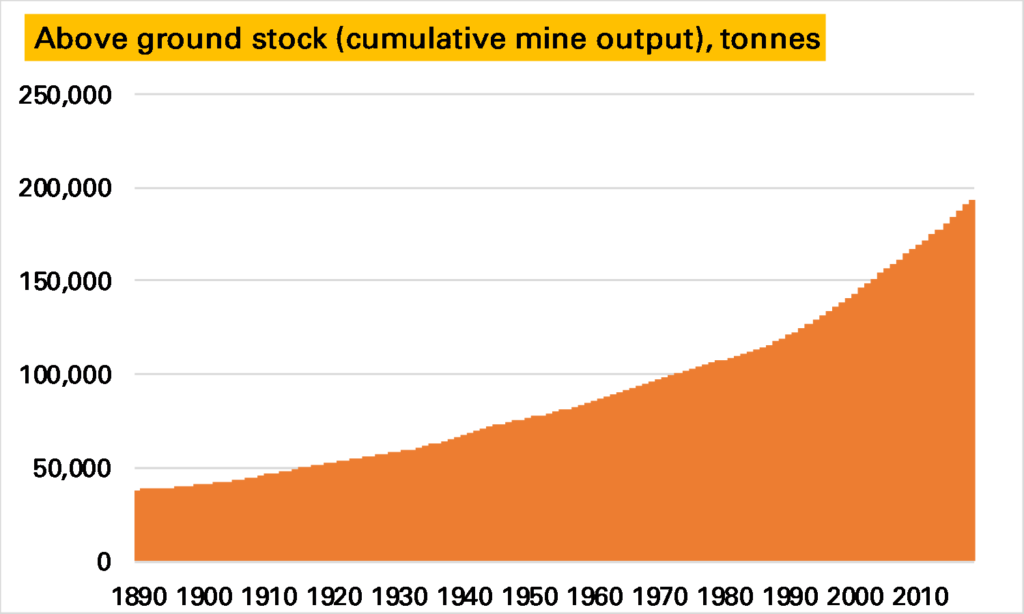

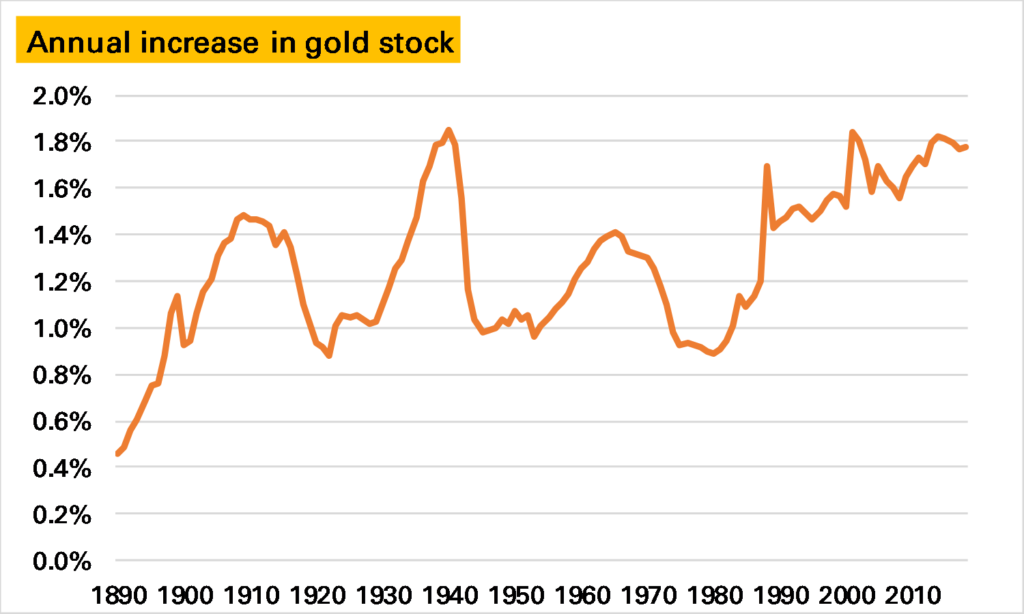

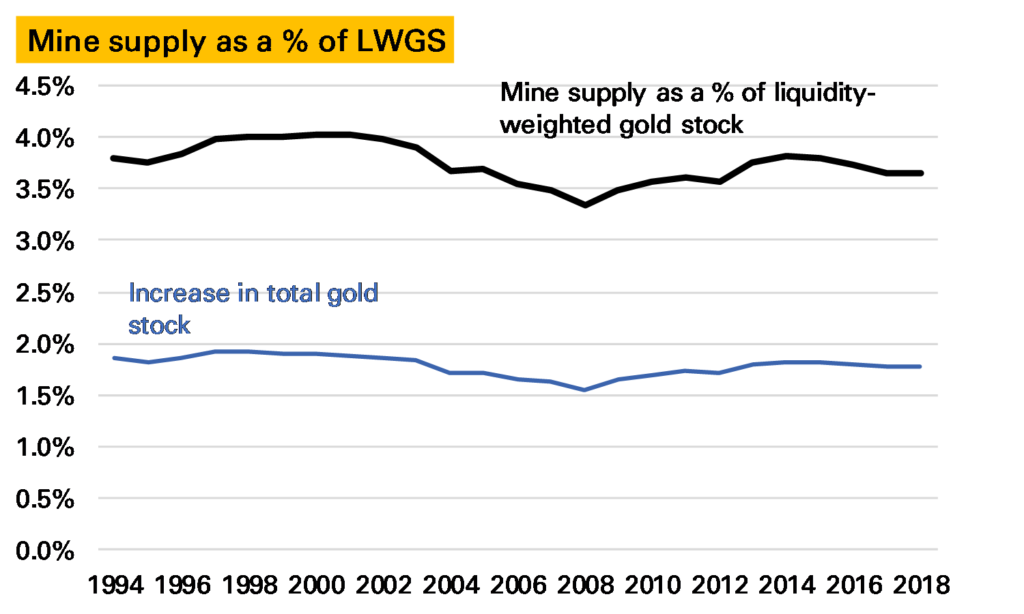

People throughout history have preferred to hold – store or wear – gold rather than consume it, and with very little deterioration very large stockpiles have steadily accumulated, rising by between 1-2% a year (see chart). GFMS 1, the research group, estimate this “above-ground stock” to be around 194,000t, some 55x annual mine supply 2.

This enormous stockpile gives (and is also a consequence of) gold’s financial-asset-like characteristics. But I’ve always thought something hasn’t quite added up about the “above-ground stocks” story. While the gold price is not very volatile compared to many other commodity prices, it seems to react far more to short-term shifts in supply & demand than you would expect of a true financial assetand given such a large inventory. To give an example, imagine all the world’s mines and wells are forced to shut 1/3rd of production for a year. The oil price would go stratospheric; gold would be far more restrained. But I think it would still go up more than a shortfall of 1,000t in a market of 194,000t would suggest 3.

How can we explain this?

One possibility is the stockpile is far smaller than most estimates. I think we can discount this. It is true the calculation is relatively unsophisticated, being essentially the sum of all historical mine production less a small assumption of gold lost forever. And it could overstate stocks if a) historical mine production has been overestimated, or b) losses have been understated, both perfectly plausible. But while over the years there have been lower calculations (see for example here), they are still many tens of times higher than current mine production; similarly even if GFMS’s ceiling of around 3,600t “unaccounted/lost” is too low 4, it is unlikely to be significantly too low.

Another explanation is that gold and gold investors are a special breed. This was suggested by Professor Anthony Neuberger in this 2001 WGC study.

Most private and institutional investors hold little or no gold. Investors who hold gold do so at least in part because gold has certain properties which make it peculiarly attractive in the event of acute political or financial instability. For these investors, gold is not readily substitutable by other assets.

In other words those who hold gold like gold as gold, not as just another financial asset, whereas most other investors don’t like gold as gold, and never the twain shall meet. Take, for example, a central bank. This argument says that hold gold as it is a unique asset of last resort, and so are unlikely to either sell it, even when the price goes a lot higher, or add more, even if it goes a lot lower. In general this means the effective potential ownership of gold is much smaller than for other financial assets, and as such the market is more internalised and hence susceptible to short-term flows.

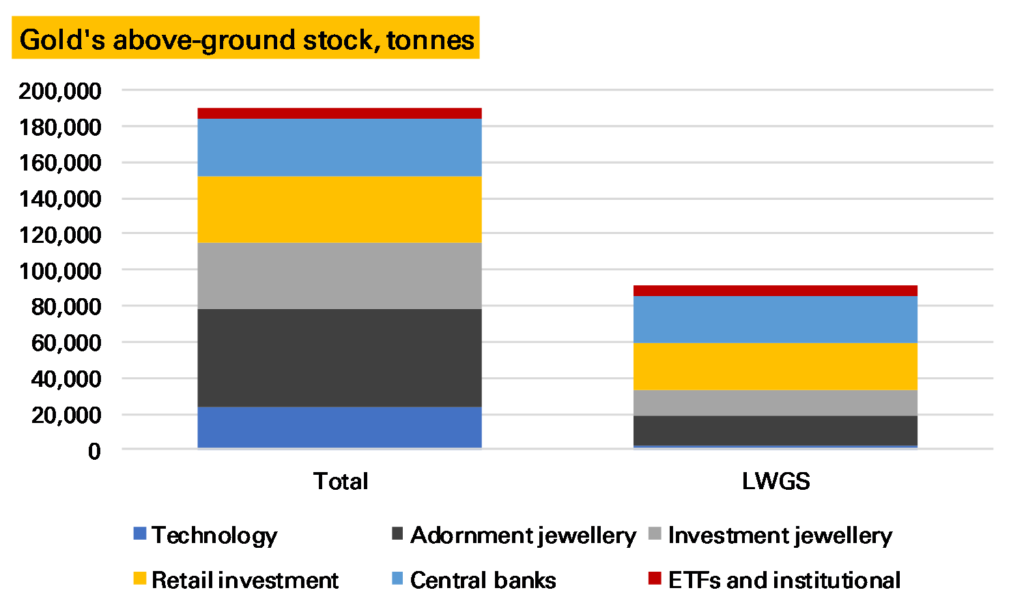

A third, and the one I want to explore, is related to both of these – that not all gold is the same. Of course we know it is held in different forms – of the 191,000t of stocks not lost or unaccounted for, GFMS estimate 5 91,600t is held as jewellery, 23,800t other fabricated products (but not coins) 6, 42,400t as private sector investment (ETFs, bars & coins) and 32,500t by central banks. My argument would be that some of this, such as ETF gold, is far more liquid than others, say certain jewellery or fabricated products and as such is likely to play a more important role in price formation.

One way to deal with this would be to exclude some of the stocks. Neil Meader, in a 2015 presentation, explored some of these issues here and offered a somewhat lower total. You could be more radical, for example, by look at the investment stocks (bars, coins and ETFs). This would reduce global above-ground stocks to 42,400t. If you added in central banks and OTC investment you would be nearer to 80,000t.

The risk here is in excluding too much. Jewellery does come back to the market and in response to price signals – especially high-carat jewellery in places like India. My alternative suggestion is that you weight each category of gold stocks in terms of how liquid they are. The idea would be that if, say, gold jewellery is being melted down and turned into bars, the global gold stock is becoming more liquid. If gold bars are being melted down and turned into jewellery, it is becoming more liquid.

Something similar happens to measures of the money supply, where the difficulty historically has been whether you should look at cash, or cash and current account, or those and savings accounts and so on (M0, M1 etc). The Divisia measure deals with this by aggregating them according to how much they provide transaction services, and its proxy for this is the relative interest rates on each type.

Unfortunately in gold we don’t have an interest rate to do that. And this is where it gets tricky. The question is how easily such gold can return to market. One measure could therefore be the cost of transforming the product into London Good Delivery metal. For ETFs this is almost zero. For bars and coins it is relatively small. For jewellery it is higher. But it doesn’t quite measure what we want. After all the cost of transforming low caratage western jewellery presumably isn’t much higher than high-carat jewellery, but it is less likely to happen as the western jewellery has higher value-added elsewhere. So possibly a better measure is gold as a % of the items value – near 100% for investment gold, quite low for western jewellery and industrial gold.

Calculating neither of these will be easy. And so I’m just going to give some guesses. I’m going to weight ETF and institutional gold holdings at 1, retail investment at 0.7, high-carat investment jewellery at 0.5, western-style jewellery at 0.3 (note I’ve made some assumptions about the split between these) and other fabricated products at 0.1. Central banks is a tricky one – they hold mostly London Good Delivery Gold, so highly liquid, but there is a lot institutional stasis preventing both buying and selling. I think the former wins out – so I’ll go for 0.8 – but I could see good reasons for a much lower figure.

Applying these weights to the current 191,000t of actual above-ground stocks gives a a weighted figure of 91,000t (which I’ll call, slightly inaccurately, the liquidity-weighted gold stock, LWGS), made up of 2,400t of other fabricated stocks, 16,500t of adornment jewellery, 14,700t of high carat investment jewellery, 25,400t of bars/coins, 26,000t of central bank gold and finally 6,100t of ETFs and other institutional stocks.

Does this aid analysis? Obviously it means for a given size of gold move the market will have a harder time absorbing it. New mine supply every year represents about 3-4% of this weighted gold stock compared to 1.5-2% of the total gold stock.

Of course while new mine supply needs to be absorbed, it is no longer an indication of how much the gold stock is growing by. That which is diverted into technological uses, for instance, doesn’t add at all much on my measure.

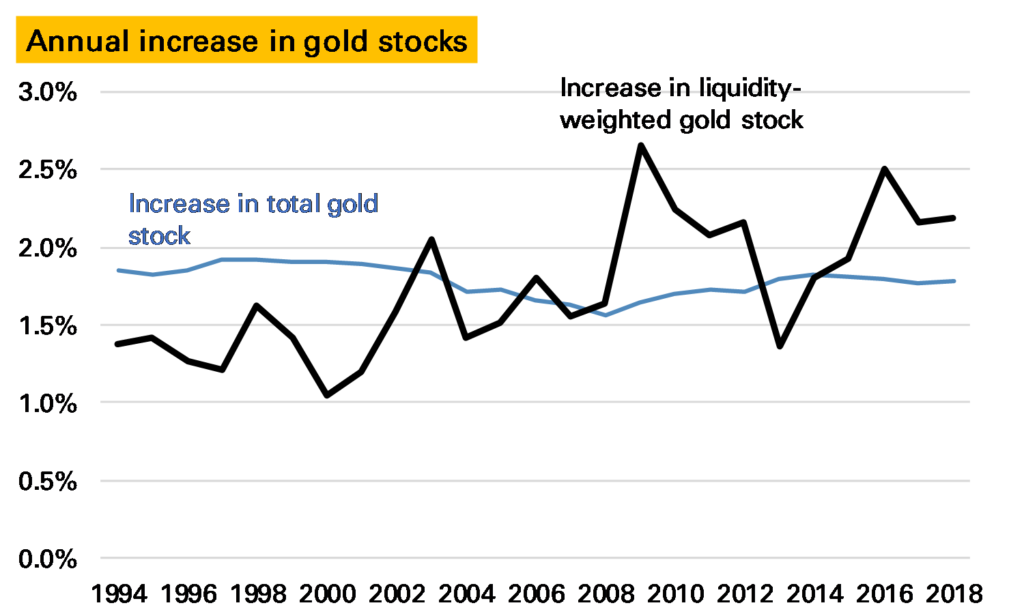

The annual increase in the liquidity-weighted gold stock looks like this.

We can see that in the 1990s the global LWGS grew less slowly than the total gold stock (or put another way the total gold stock was becoming less liquid), a function largely of liquid central bank gold being sold and converted into less liquid Asian jewellery. But starting in 2001, and gradually building up to 2009, the annual increase in this liquidity-weighted gold stock accelerated as this process reversed, with a splurge of investor buying. Since the the liquidity-weighted gold stock has continued to grow proportionally faster than the total gold stock, with the exception of 2013, when a wave of ETF selling saw liquid gold melted down and converted into less-liquid jewellery into China.

Notes:

Note all the charts in this piece are based on GFMS Refinitiv supply/demand data, with historical data from the USGS ↩

The only slightly comparable commodity would be silver – see here for a new look at its inventory ↩

A similar argument can be made if gold demand was to fall by 1,000t suddenly – in theory investors should rush in from other assets – in practice I think the price would fall substantially ↩

And it oddly hasn’t changed in nearly two decades, I think ↩

Compared to the total stock these breakdowns are evidently more open to error ↩

I’m a bit puzzled what this is, to be honest. The bulk of industrial demand is electronics, at around 300t a year, which would account for this but surely much of that is thrown away or recycled? ↩

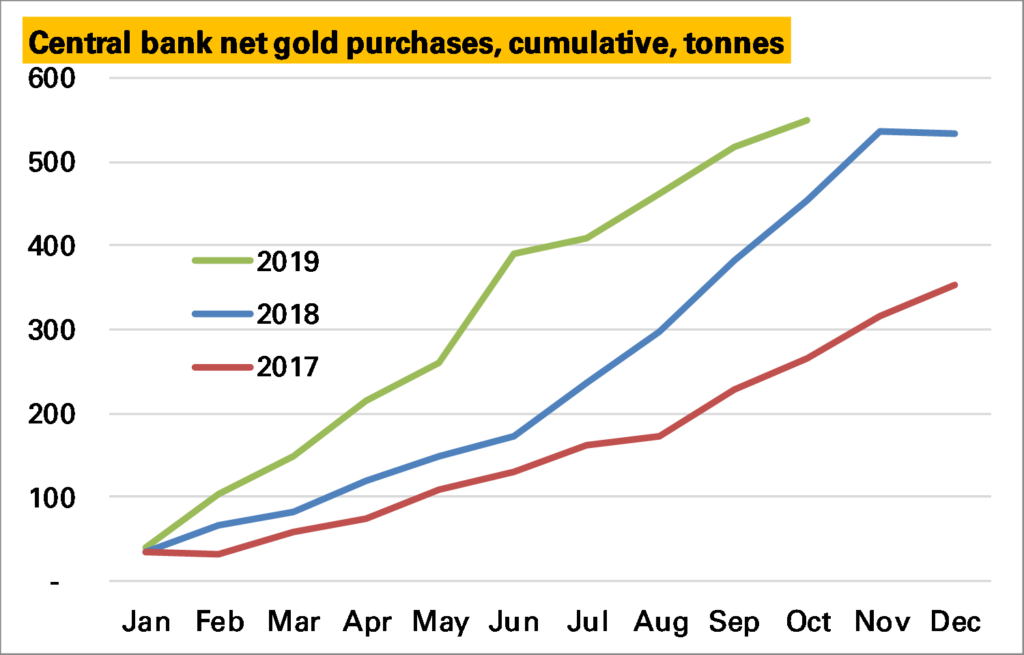

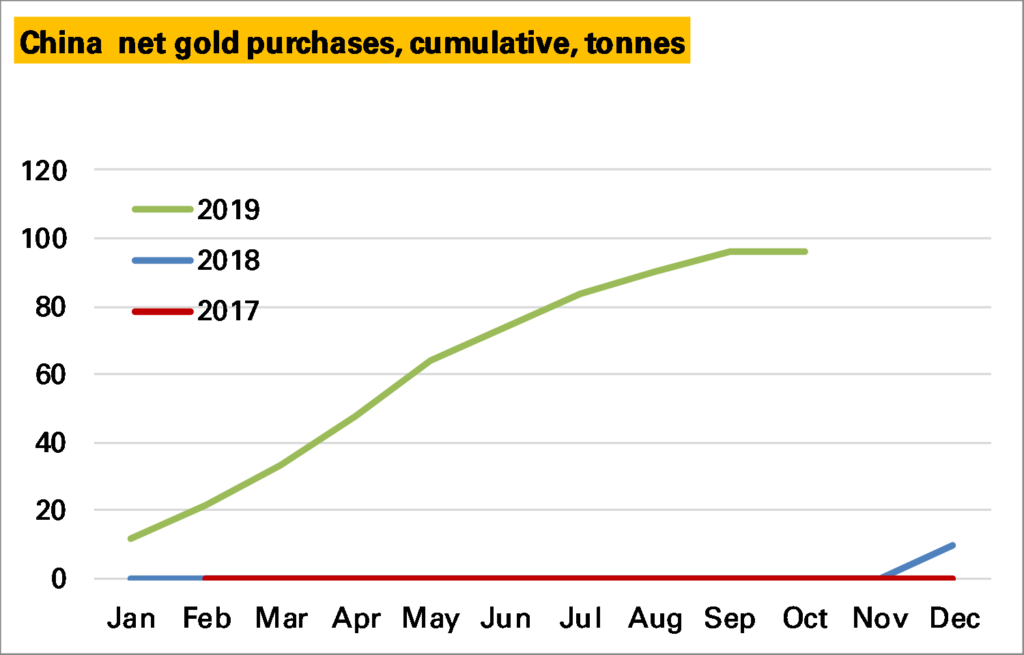

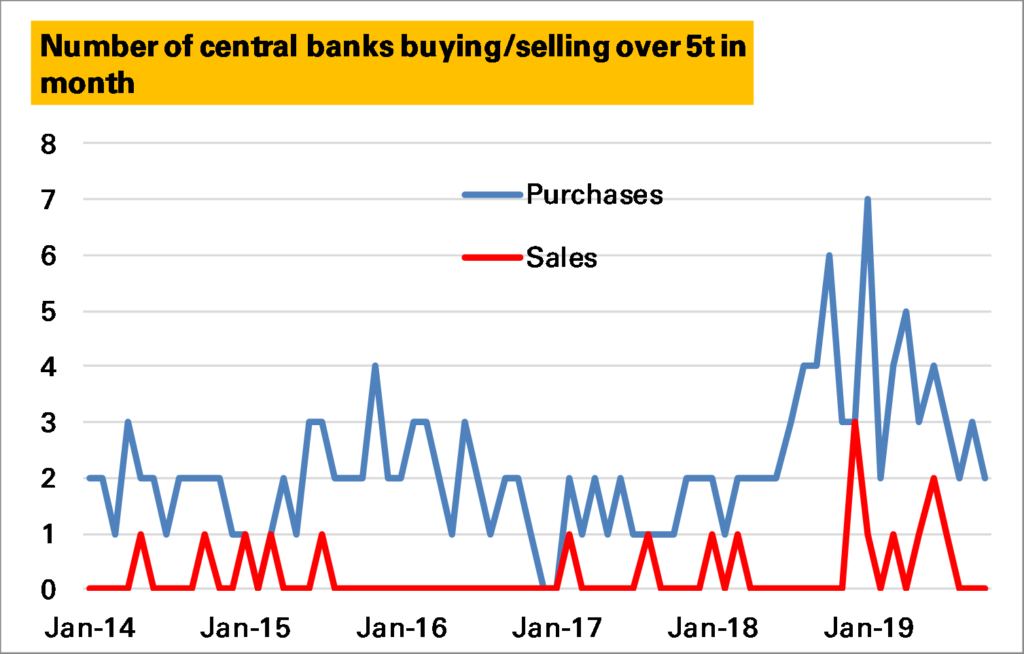

As of October, the latest available data for most countries, there has been a net addition of 550 tonnes to central bank reserves, 17t more than in the whole of 2018 and far ahead of the amount seen in 2017.

Purchases are slowing, however. By the end of the first half of 2019 net purchases had already reached 390t, an average of 65t/month. In the last four months 160t have been purchased, a slower 40t/month. This figure might rise a little – some countries report late, and the trend tends to be higher – but is unlikely to change much.

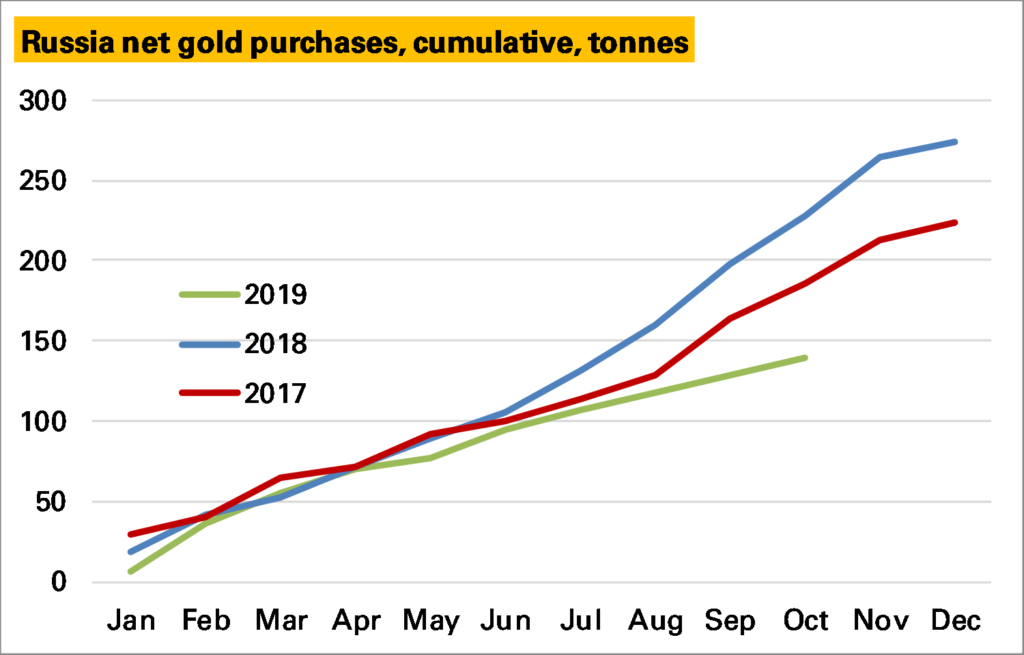

To what extent is this a concern? A key reason for the H2 slowdown is Russia, the bedrock of global central bank gold accumulation. Here purchases in 1H were broadly inline with previous years, but since then have been much more muted. This is in line with a new policy adopted by the Central Bank of Russia to reduce gold accumulation and has meant an increased rate of Russian gold exports. As such it looks set to be a drag on the global total going forward, albeit one that was inevitable at some point.

Also helping purchases in 1H 2019 was a resumption in Chinese central bank gold buying after a few years hiatus. This too seems to have slowed a bit in 2H but it is too soon to know whether October’s zero purchases marks another cessation of buying or is a temporary pause.

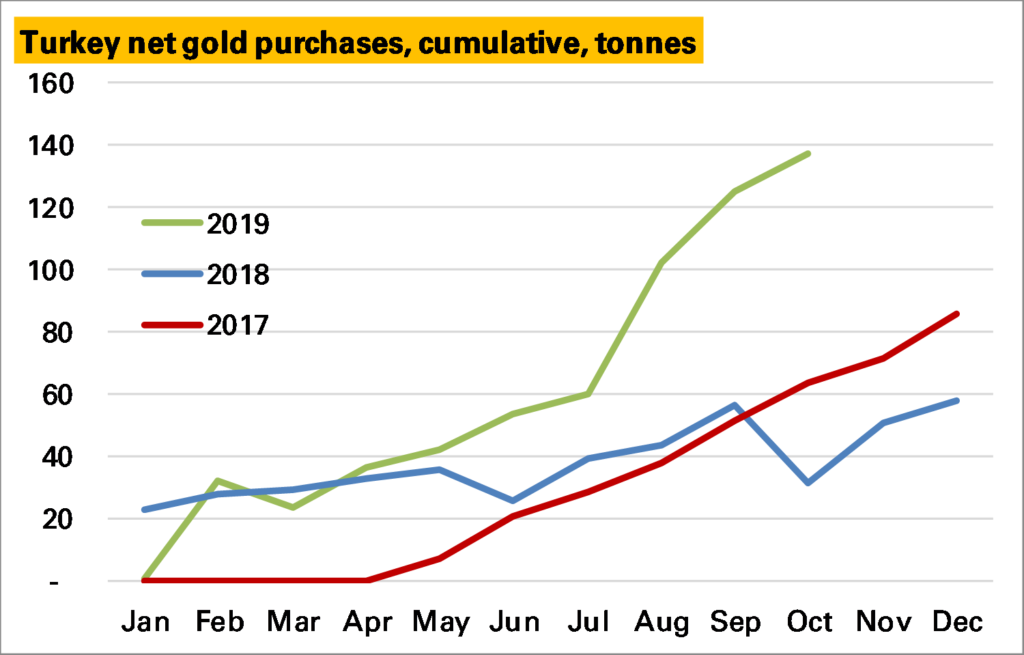

What has prevented an even more rapid slowdown, however, has been an acceleration in purchases from Turkey – on nearly 140t YTD, far higher than in previous years. Whether this will continue is a difficult one to call. Turkey’s central bank gold policy is somewhat confusing given they also hold private-sector gold against reserve requirements (these numbers exclude that), but there has been a policy shift in favour of gold in recent years.

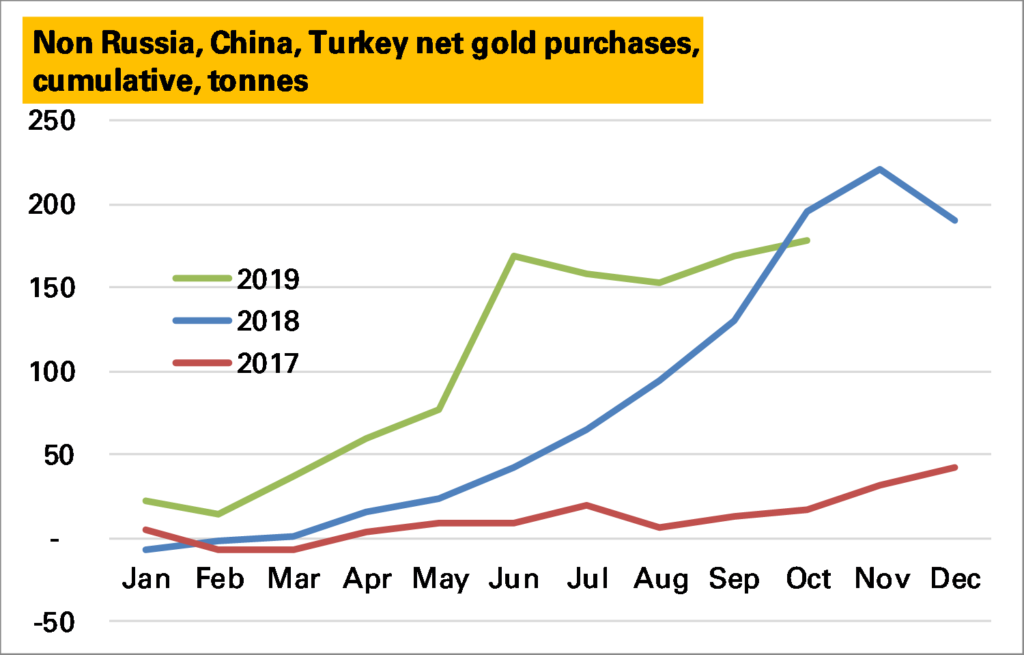

Finally, there is the Rest. And in recent years these have been the great hope of the gold market with a number of big purchases, particular in Europe from Hungary and most impressively Poland. In 1H 2019 other countries added 160t of gold, far more than ever before. In 2H so far barely 10t have been added. However the nature of these purchases mean that they tend to be lumpy.

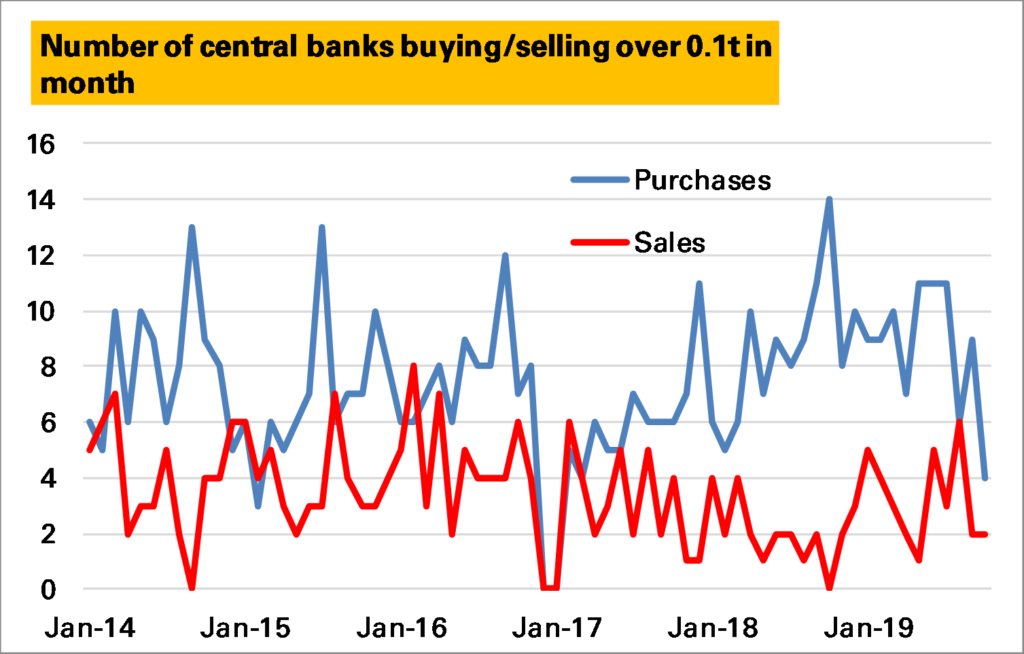

Indeed if we look at central bank activity, here shown as the number of central banks buying or selling in a month, we see an increase through 2018 in purchases, and a decline in sales, which has since reversed (note I’m excluding the BIS here, correctly, and Turkey, incorrectly, which in most months would add 1 to the purchases line).

If we choose a less granular measure, say 5t/month, the trend is even clearer (note exceptions above).

Source (all charts) – IMF and national central bank websites

So it does look as if there has been a slowdown in central bank buying, and not just because of Russia, which is the biggest impact. One explanation could be the high price, which might make the case for switching into gold harder to explain. But its worth remembering that the pace of buying in 1H 2019 was unprecedented, and current rates are still quite positive. The main concern I have is that Turkey is unlikely to be as reliable a buyer as Russia.

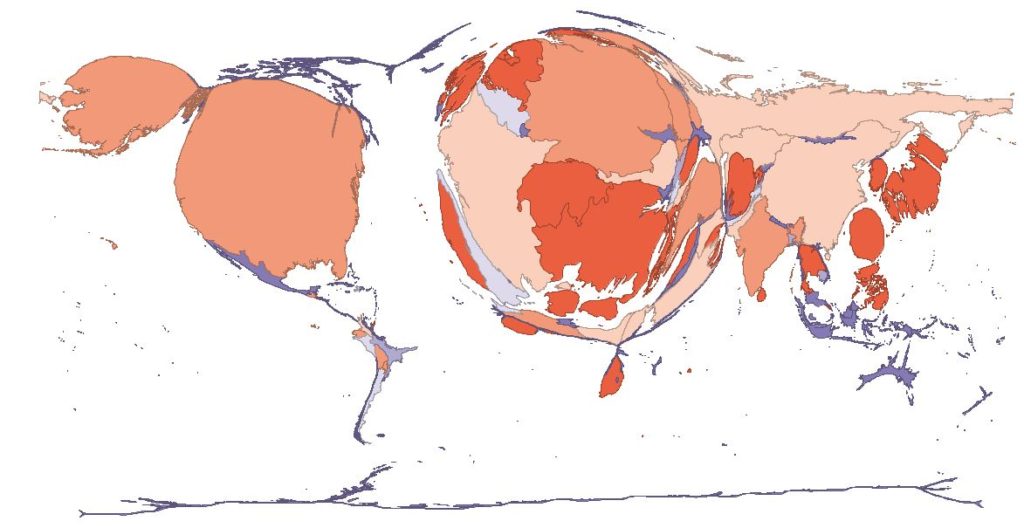

Over time this remains a positive part of the market, and I expect central bank purchases to continue, not least because of the imbalance in global holdings shown here (each country is resized to reflect the size of its gold holdings). For more details see here.

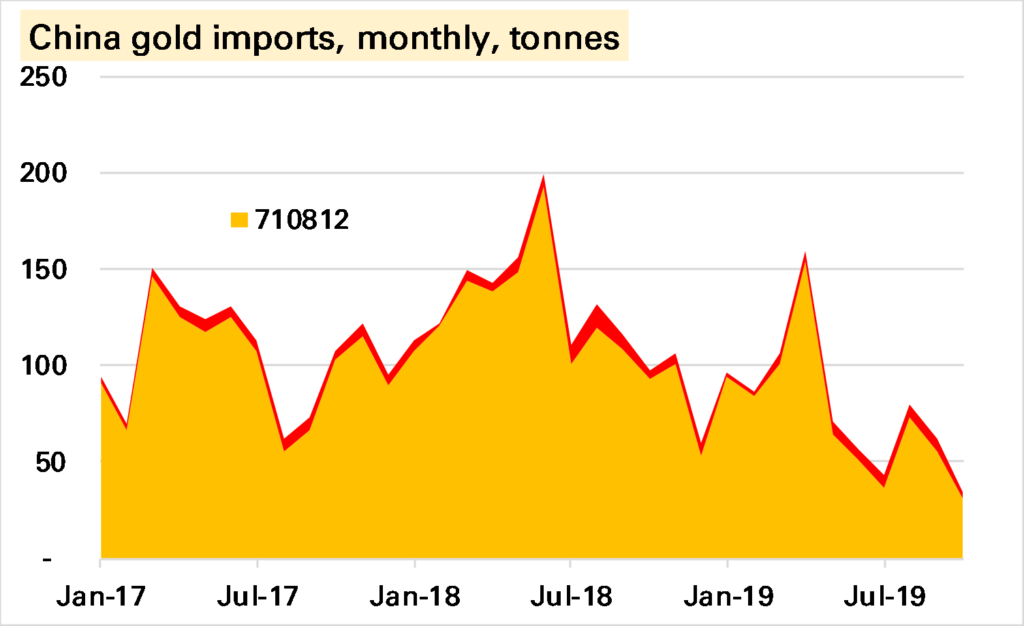

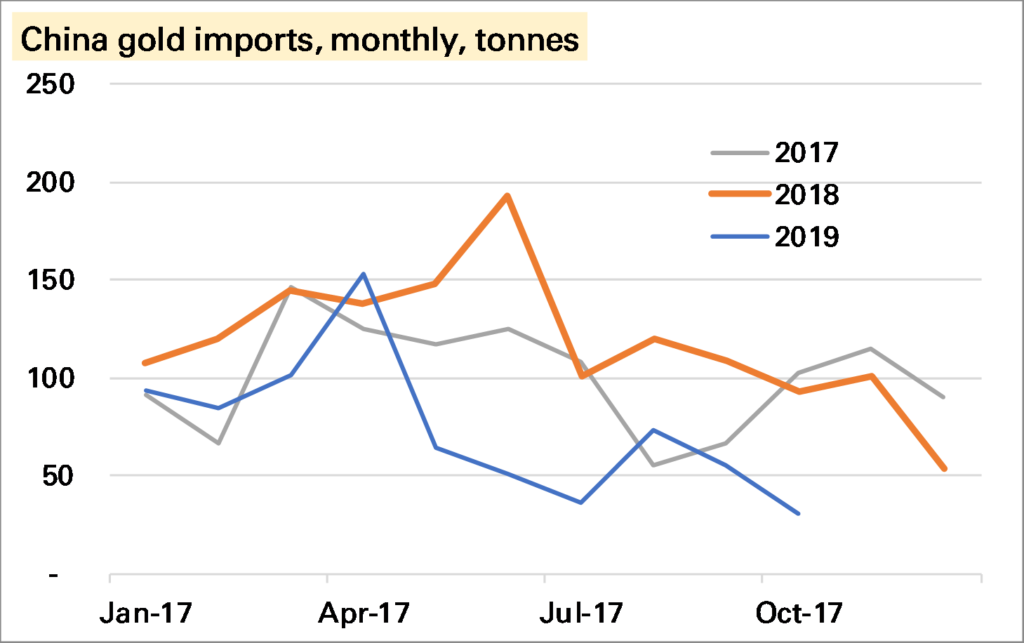

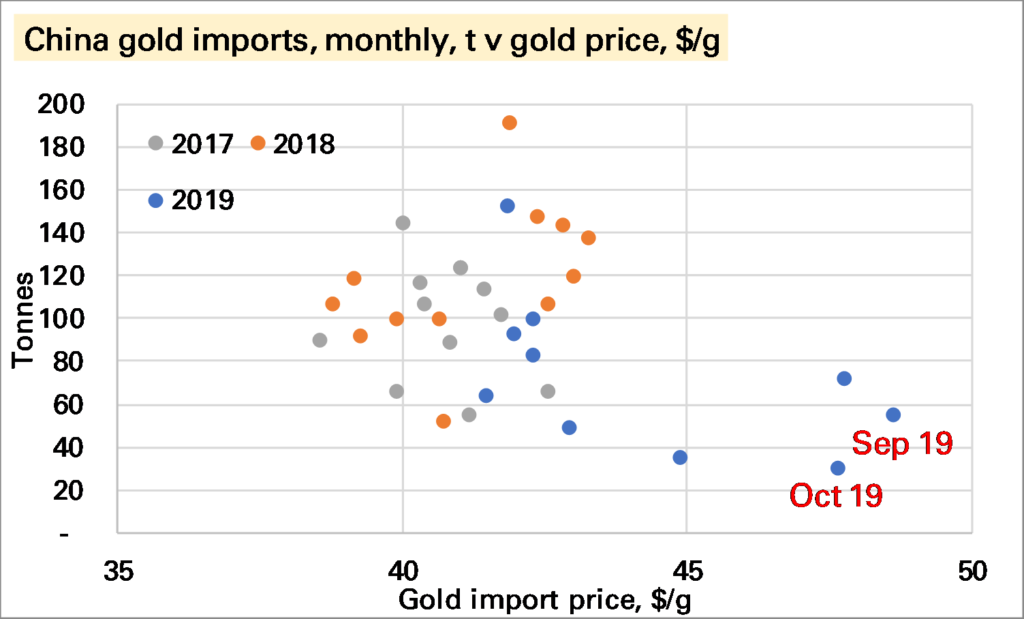

China imported just 35t of gold in October, the lowest monthly amount since it began reporting official trade data from January 2017. Seasonality must have played a role given holidays in October. But while the trajectory of imports looks a little similar to 2018, it is at a far lower level.

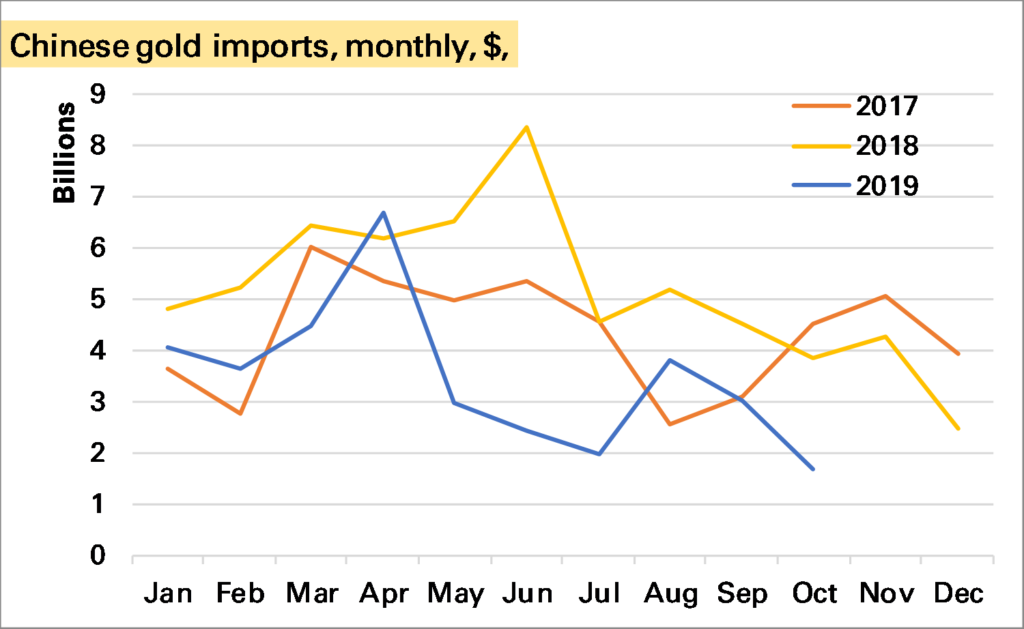

The high gold price is another factor. The first chart below shows that imports in the last two months have been made at by far the highest price in this data series, and arguably are not out of line with previous trends. In terms of the amount of money spent on imports the trend does not look as poor as for the volume (second chart below) though October was still a poor month.

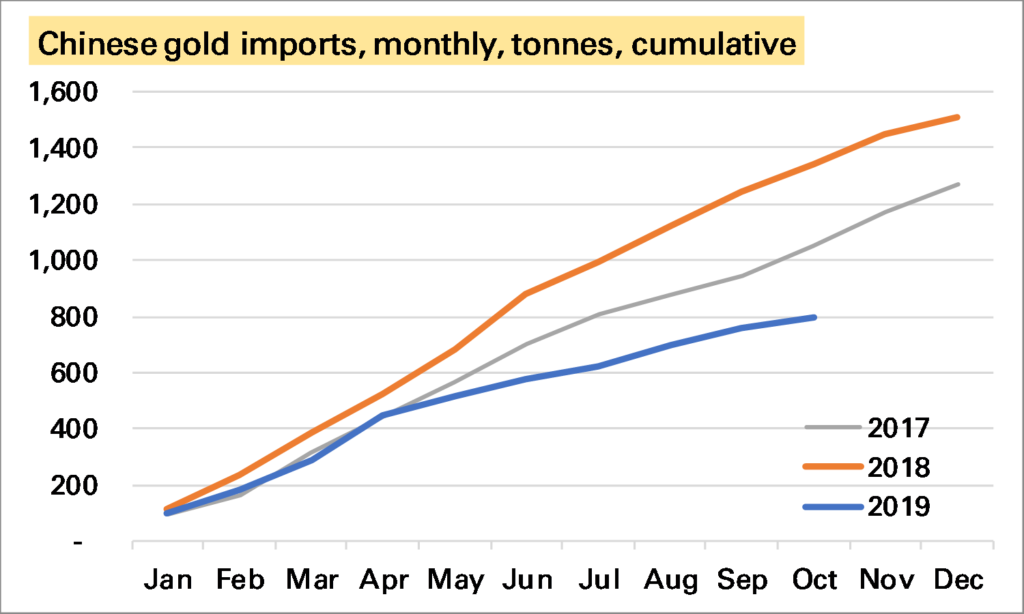

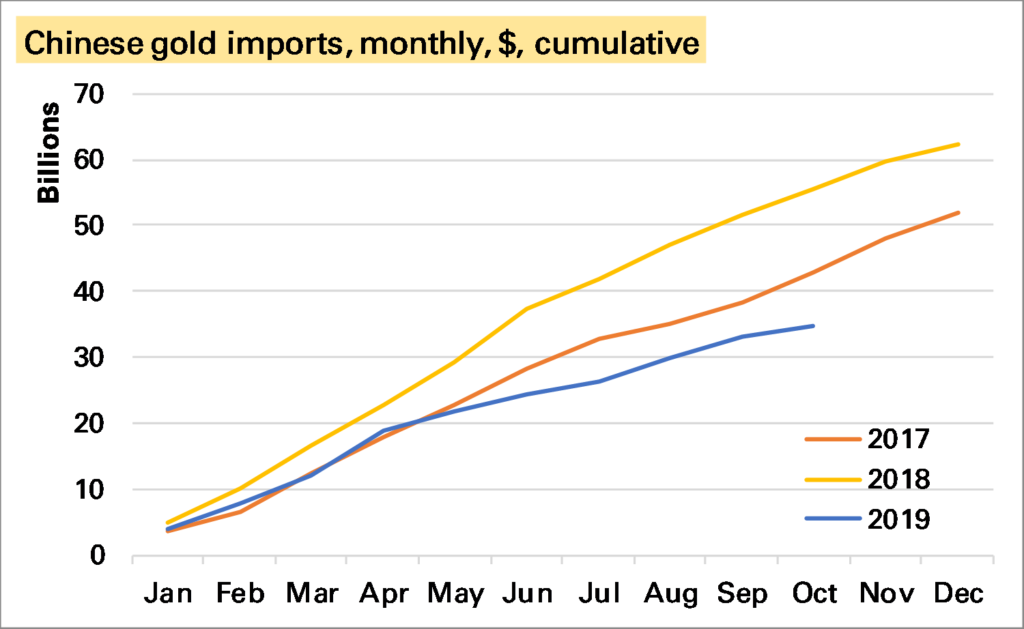

Year-to-date gold imports are now around 800t, well below the levels seen in the last two years. In terms of money spent the gap is narrower – and perhaps not too bad given the restrictions placed on imports earlier in the year – though again October does stand out as suggesting a worse trend.

Source: All charts – China Customs. Note click on chart to enlarge.

To what extent does this matter? It’s possible China is importing gold in other forms such as jewellery, or there are more unofficial imports going in. Even if not (Western) investors have been buying a lot of gold, and despite all the talk of gold stockpiles, this tends to mean the Chinese can’t have as much. The price rises to see who wants it most and typically it’s the investors.

But… the biggest risk to the gold market medium-term, in my view, is lacklustre”physical” demand, of which over 50% comes from China and India. In particular it seems to me that gold – both as a consumer good and an investment good – now faces far more competitors (eg smartphones, index-linked bonds) than it once did. Of course some of its qualities are unique and it has a long track-record, suggesting a certain robustness.

That the dollar spend on Chinese gold imports is declining could be another warning sign.

For the background on how China now publishes gold trade data see my LBMA Alchemist piece from earlier this year.

I don’t like monthly YoY data. For sure it has its advantages, in particular seasonality is normally dealt with. 1 But as a guide to what happened in the month in question it it rather lacking.

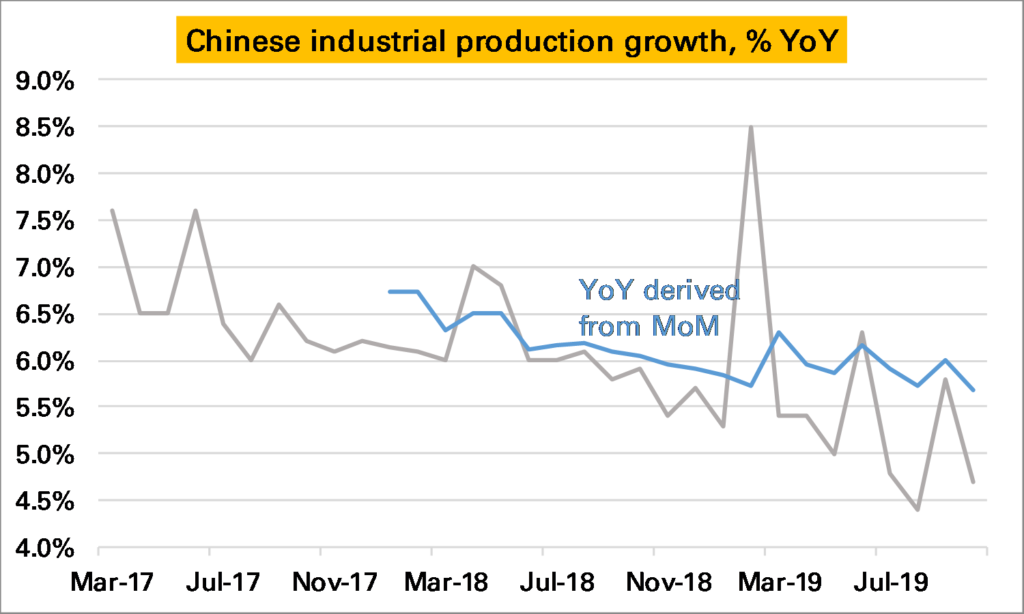

Chinese industrial production, an important datapoint for commodity demand (and the wider global economy), is normally reported as a YoY series. This has slowed steadily, and in October was just 4.7% higher YoY, a sharp slowdown from the 5.8% growth seen in September (grey line in 1st chart). However it remained higher than the low of 4.4% seen in August.

The probem with a YoY series is we don’t know whether October was a bad month, or October 2018 was a very good month, and similarly how it compares to September.

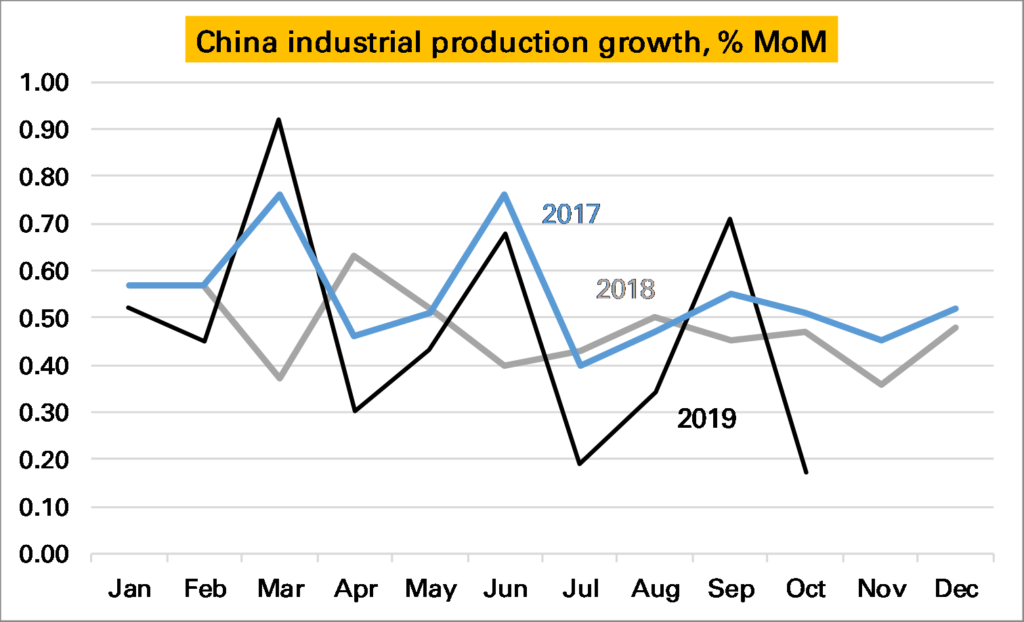

Luckily for IP, China also publishes a seasonally adjusted month-on-month (MoM) series. It doesn’t get much attention but in theory should give us a much more accurate read on how the industrial sector is doing at the moment. If so it looks very bad news – October saw growth of just 0.17% a month. This is the lowest monthly print I can remember, and as the following chart shows certainly the lowest in the last three years. If maintained for the next 12 months Chinese YoY IP growth would be just 2%.

But the chart above also shows something else – the seasonally adjusted monthly growth rate appears rather…seasonal…especially in 2019. The first month of each quarter has been weak, and the last month strong. As such it looks like November’s print is likely to be around the same as in 2018 and December’s much stronger than in 2018. This would mean the YoY rate should stay around the same in November and rise strongly in December.

There lies one more complexity. The YoY rate derived from this monthly data does not equal the YoY rate reported by the NBS. The first chart shows the former in grey and the latter (headline) in blue. Even with the weak October monthly print the derived YoY remains above 5.5%.

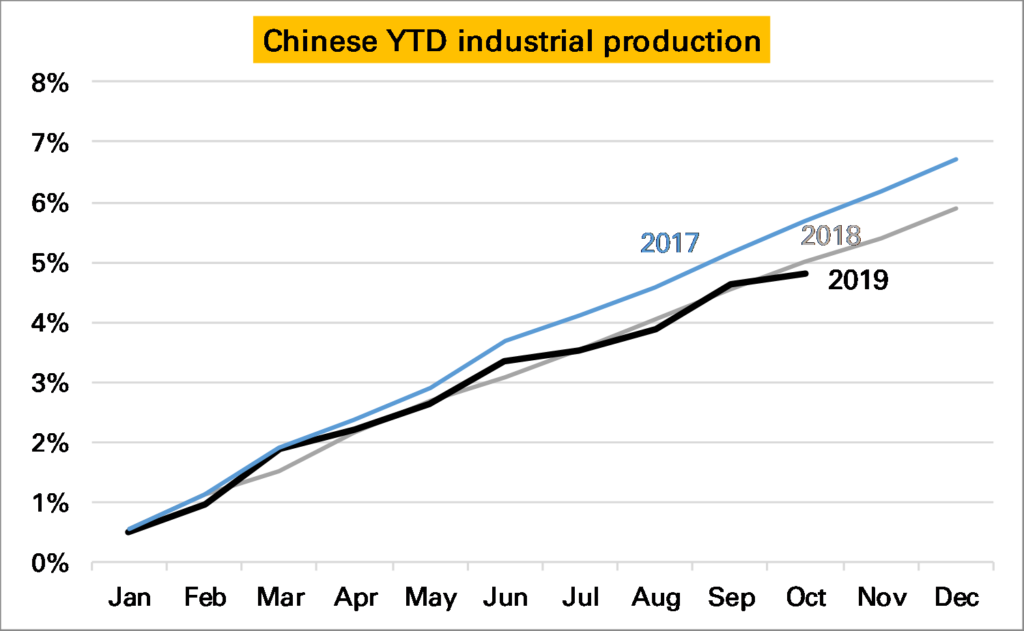

Where does that leave us? Chinese IP growth is slowing, though the YoY series might overstate the severity of the slowdown. October was a bad month, but November and December are likely to be better given the 2019 pattern so far. Given so much confusion I cling to my chart of YTD growth in industrial production derived from the monthly data. The pattern is less smooth this year but overall output has grown much the same as in 2018.

Notes:

An obvious exception being shifting annual holidays such as Chinese New Year or sometimes Easter ↩

A slump in Chinese electric vehicle (EV) sales drove global EV sales into reverse in October. I estimate, using national and other sources, that 130k EVs were sold during the month (140k if you include Chinese commercial vehicles), 32% lower YoY, with both battery-electric vehicles (BEVs) and plug-in hybrids (PHEVs) down a similar amount.

The sharp global YoY fall is partly because in previous years sales have risen into year-end on a combination of beating expiring incentives and a generally rising market. But sales last month were also lower MoM, and while this owes something to wider market trends, it is mostly due to China.

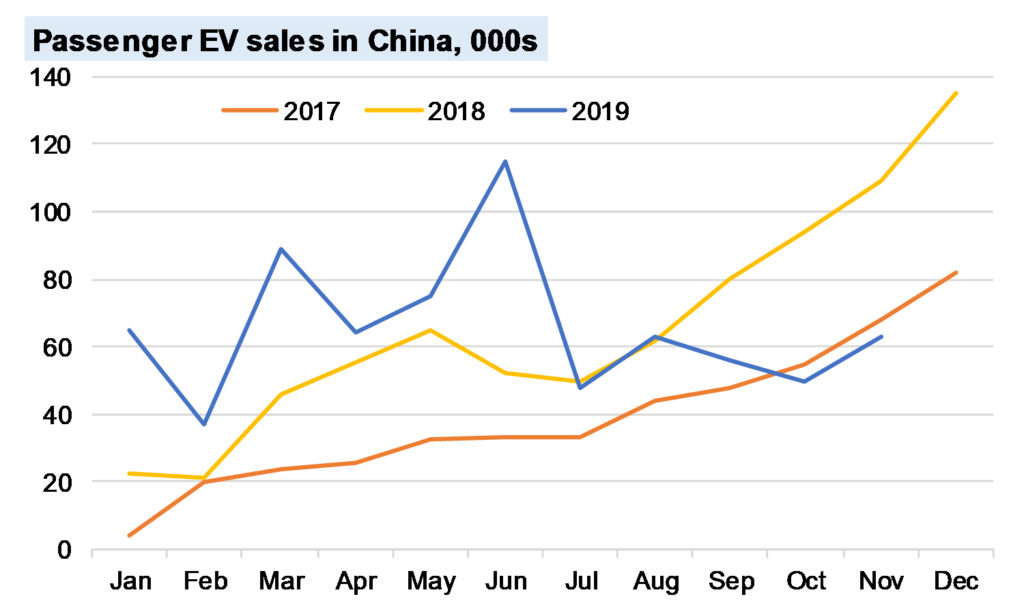

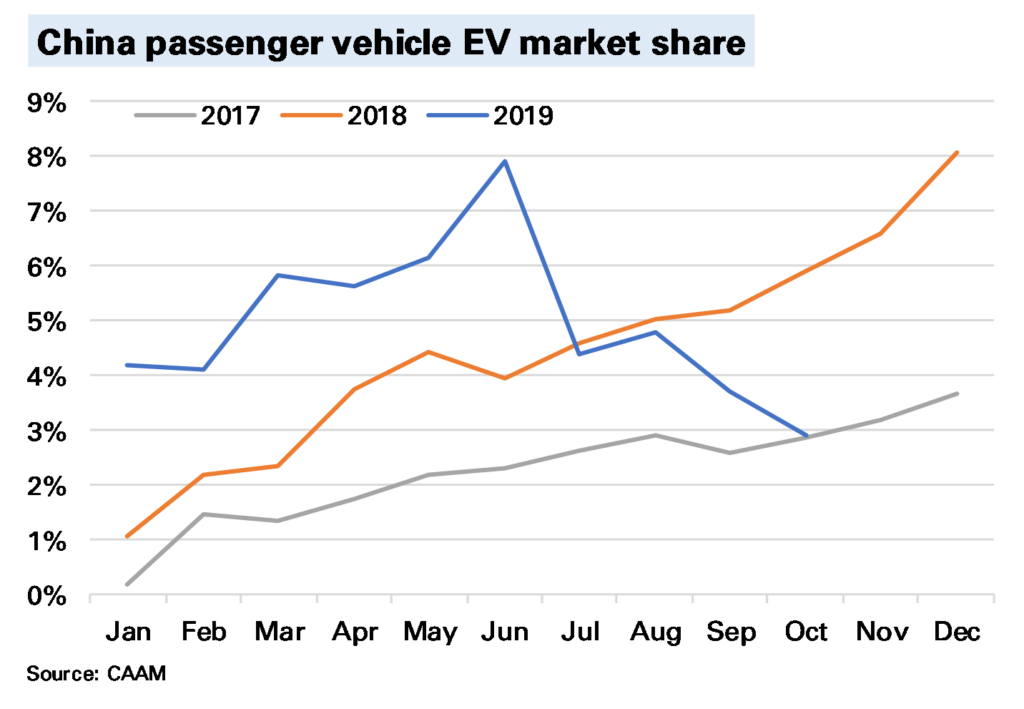

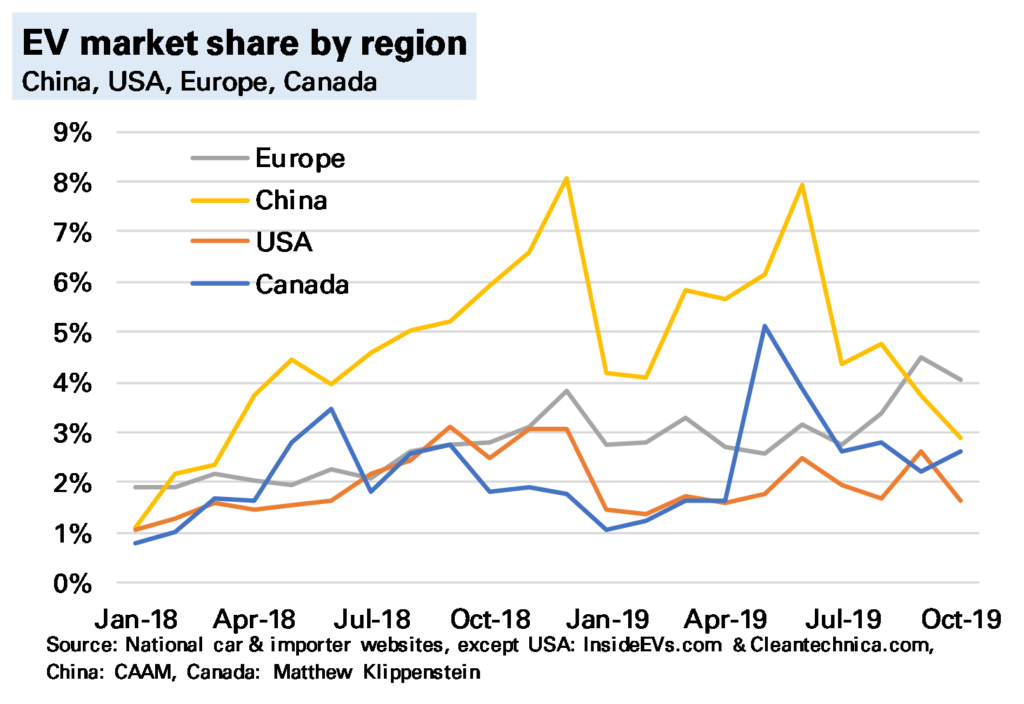

In China, which accounted for 64% of global EV sales in October 2018, EV sales were 54% lower YoY, with BEVs down 47% and PHEVs down 78%. The following chart shows this is not primarily related to a weakening wider market (all passenger car sales were down, but a more modest 6%) but a sizeable fall in market share. The reasons for this we’ve discussed many times before, and are mostly subsidy-driven, though the extent of the slump does point to some consumer disenchantment. Sales for the full-year are now only 18% YoY higher YTD and could end the year lower than in 2018.

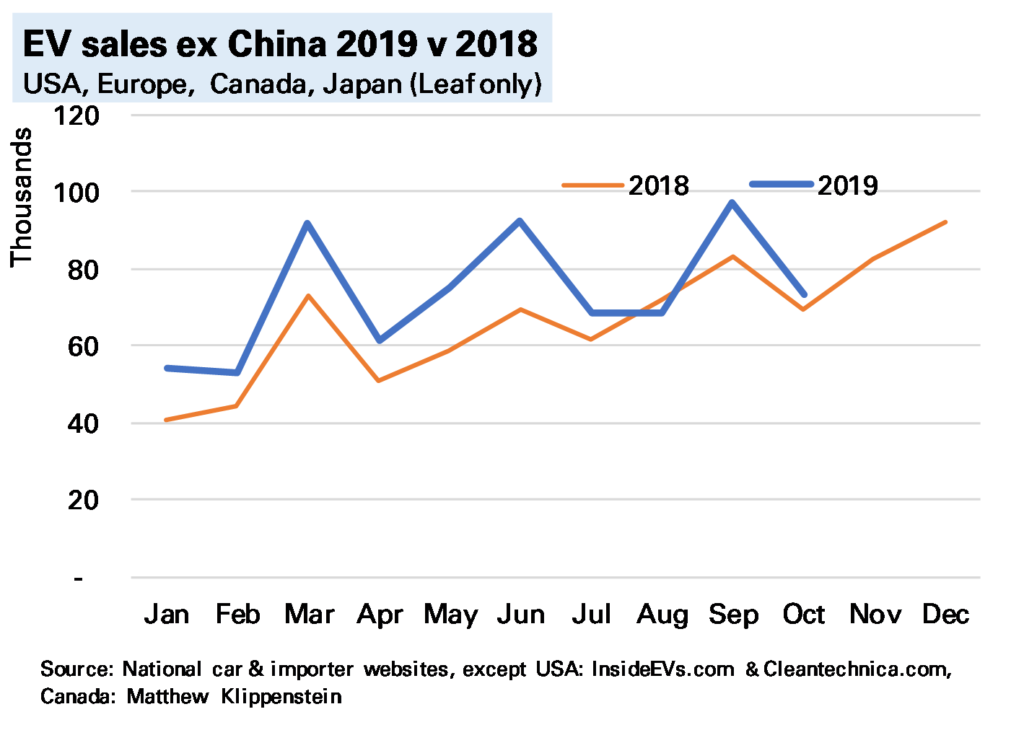

If we exclude China then global EV sales were still slightly higher YoY, though note not by much.

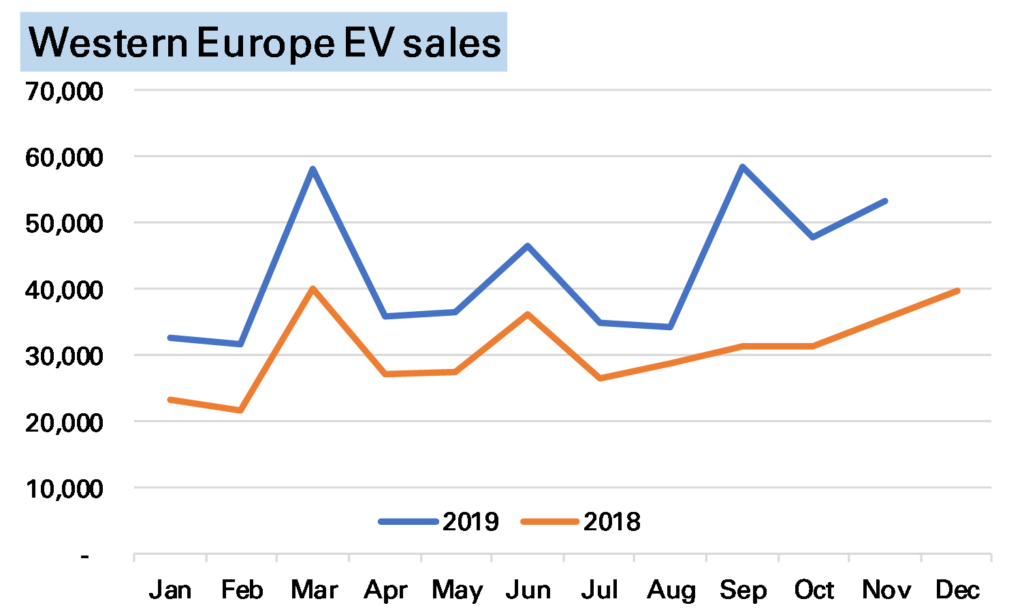

The only bright spot at present is Europe (see my earlier post), where sales were more than 50% higher YoY. And while total EV sales in Europe were still lower than China in October (48k to 56k) the gap has narrowed considerably, and in terms of market share of all car sales Europe has now been higher for two months. Of course this owes something to the Tesla Model 3 roll-out, which is likely to subside, but it does suggest the dominance of the Chinese market in sales is not as obvious as once seen (of course production & battery manufacturer are different questions).

I’ve not said much about the USA, and for two good reasons. One, sales seem subdued, with Tesla concentrating on foreign markets. Two, we are lacking accurate data. The sterling work done by sites such as www.insideevs.com and www.cleantechnica.com in assessing this continues, but a decision by most manufacturers to switch to quarterly data 1 means much monthly data is now guesswork, and for PHEVs I’ve had to make an extrapolation on previous trends. This won’t make a change to our global conclusions – the US does not have a big enough market – but it does mean we need to be cautious on assessing the micro-trends.

My view on the longer-term outlook remains the same. The current slump is a reminder that technological shifts are rarely smooth, and some of the reasons for it (subsidy-issues, consumer reluctance) also point to why EV roll-out will be slower than the more bullish predictions. But subsidies are not all one way – the German government recently announced more generous ones – and consumer reluctance will be overcome by a wider and better range of models. And 2020 still seems a crucial year for that.

Notes:

There is no national or govt tabulation as in many other countries ↩

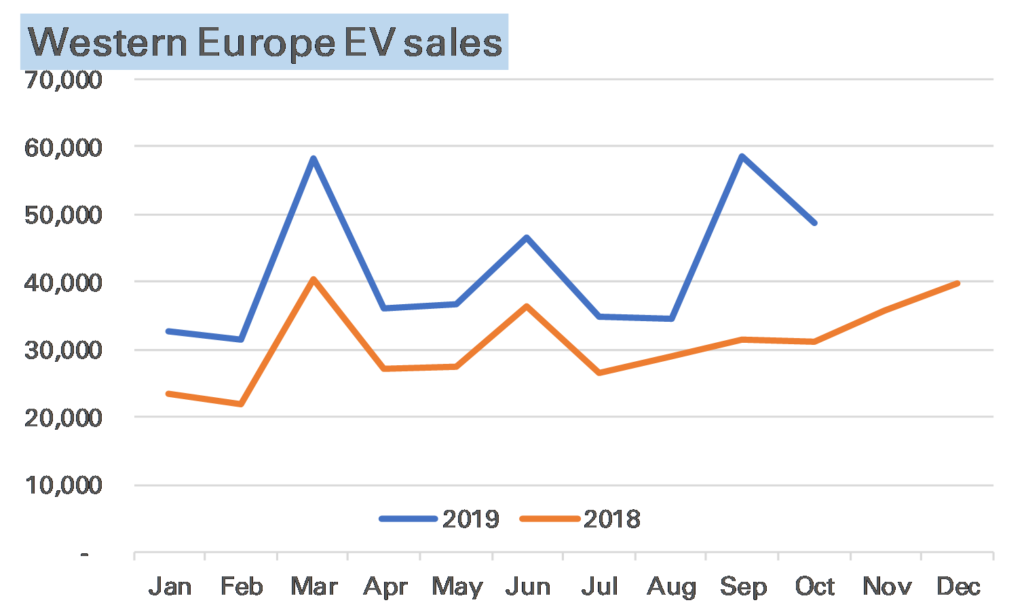

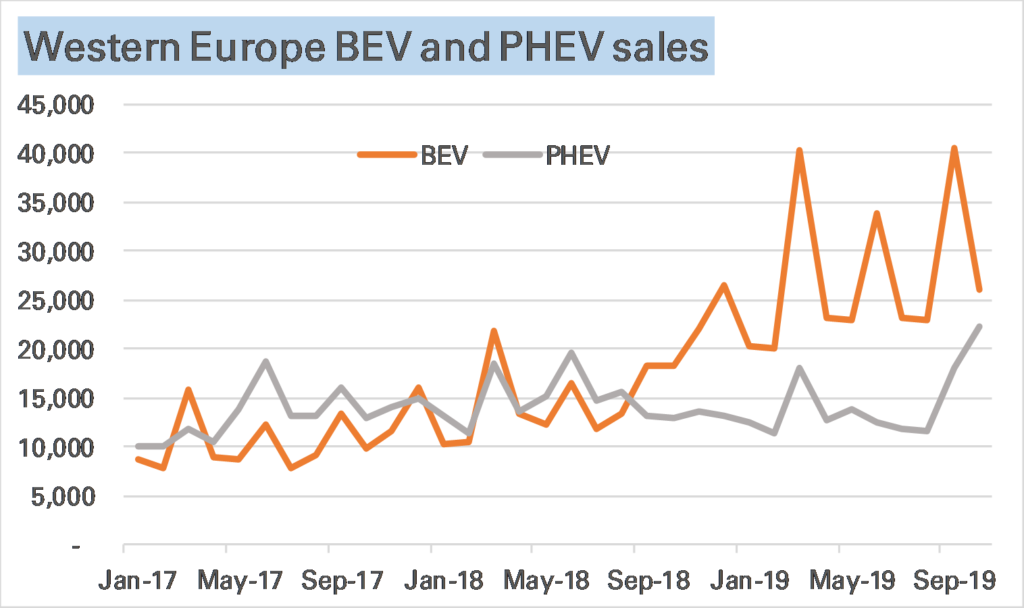

Using national sources I estimate European EV sales were 56% higher YoY in October, with just under 50,000 sold, a market share of around 4%.

Sales were lower than in September, partly a result of the normal trend of European car sales (the UK’s biggest month is in September due to number plate changes) but also because much of the pent up demand for Tesla Model 3s has now been satisfied.

Indeed given this that sales did as well as they did was impressive and due to an unusually high number of PHEVs being sold (see charts 2 and 3), especially in Germany. I don’t have the model breakdown yet to see exactly why this happened. Normally in EVs big changes are subsidy related, but German subsidy changes came only recently and more likely it reflects German marques having released a lot of new PHEV models recently as they are seen as a good way to meet the WLTP test restrictions.

YTD new EV registrations are up 42%, almost spot on my rule-of-thumb growth forecast of 40%.

September’s Macedonian trade data is out, important for PGM market participants as it is the best way I can come up with to track whether super-expensive palladium is being substituted out of the diesel catalysts for cheaper platinum 1.

So far there has been no evidence of such substitution, indeed the palladium ratio of the two metals has actually trended higher through most of this year.

September was a little different. Imports of both metals plunged, but because palladium fell more sharply, the implied ratio did move in platinum’s favour, to 36% by weight, compared to 44% in August’s data.

Source: UN comtrade, Matthew Turner, November 2019

But it’s way too soon to read anything into this. 36% is actually the six-month average, and higher than seen in many months this year.

The sharp fall in imports of both metals is quite interesting. It seems unlikely there is going to be sharp fall in output so one suggestion that comes to mind is metal was being stockpiled ahead of potentially disruptive “no-deal” Brexit (the metal comes from the UK), though that is guesswork.

What is clear is the imported price of palladium is rising fast. In September it was $1,570/oz, the highest on record. That corresponds to the market price in the first part of the month – October’s was much higher.

Notes:

For details of why this is the case, which in short because Macedonia’s main importer is a huge JM catalyst factory, see here↩