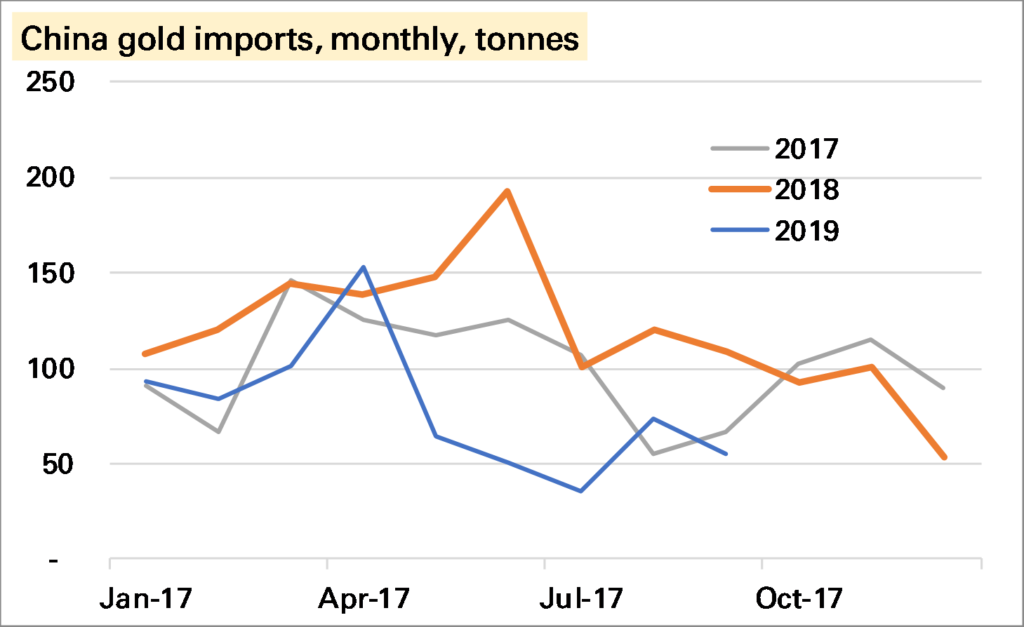

China imported 62t of gold in September, according to recently released customs data. This is slightly down on last month, above the lows of summer, but subdued compared to earlier in the year and in 2018.

Source (this and all other charts): China Customs, SGE, Matthew Turner, October 2019

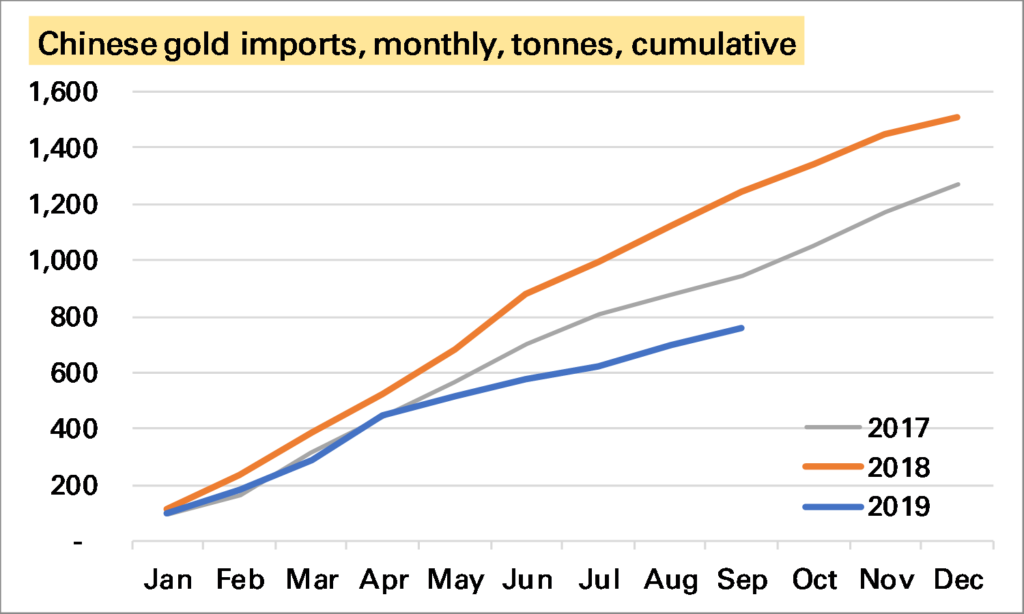

Gold imports in the first nine months of the year have totalled 760t, more than a third lower than the 1,242t seen at the same point of 2018.

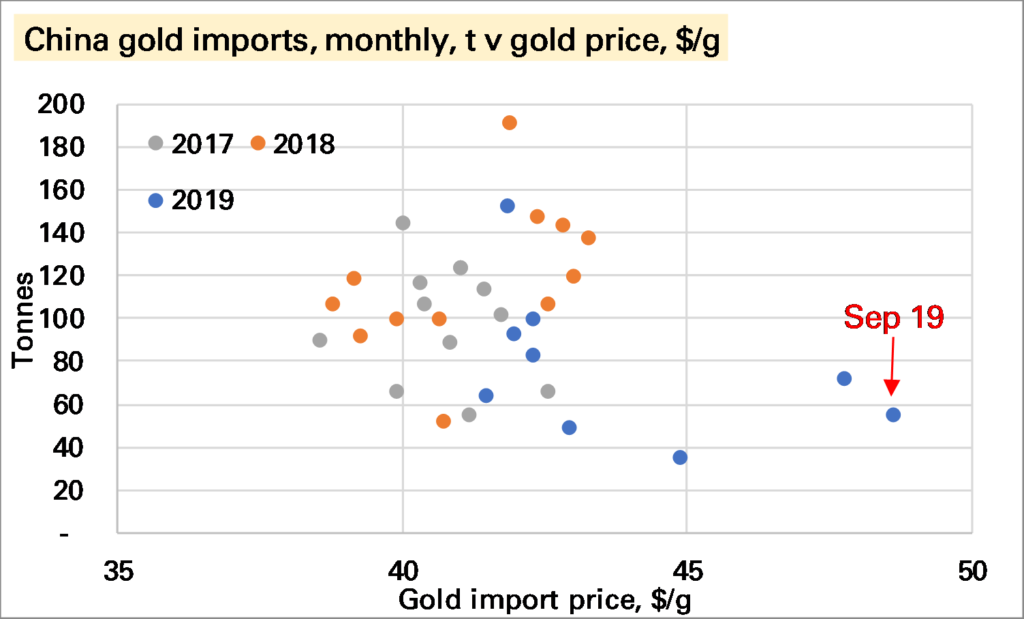

Of course one factor is the much higher gold price, with western ETF investors bidding up the price.

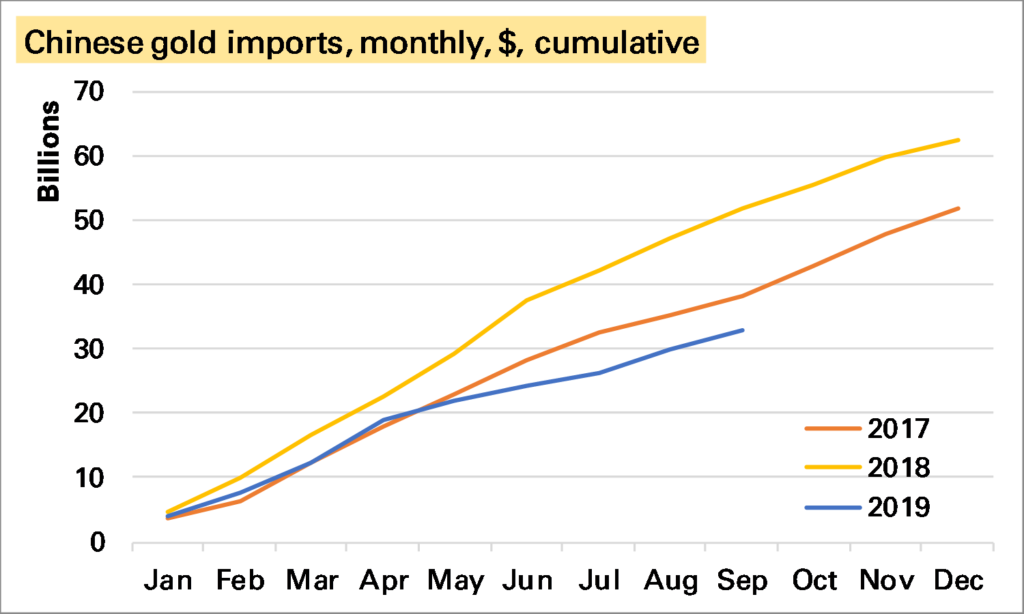

But in terms of value of gold imported 2019 is also proving a weaker year than 2018, and even, since the start of summer, with 2017.

Is this something for the bulls to worry about? This Reuters story placed the blame for the very weak summer period on quotas restrictions aimed at restricting the outflow of Yuan. These were apparently eased in August, helping explain why imports have picked up a bit. Presumably at the LBMA conference in Shenzhen more was said about this. Such restrictions do suppress gold demand but if only temporary are unlikely to do lasting damage.

Furthermore there is a real sense, despite all the talk of gold being a 200,000t “stock” market, that if ETF investors are buying a lot of gold, the Chinese can’t have as much. The price rises to see who wants it most. So it’s certainly not as concerning as it looks.

Nevertheless it remains concerning. The biggest risk to the gold market medium-term, in my view, is lacklustre”physical” demand, of which over 50% comes from China and India. In particular it seems to me that gold – both as a consumer good and an investment good – now faces far more competitors (eg smartphones, index-linked bonds) than it once did. Of course some of its qualities are unique and it has a long track-record, suggesting a certain robustness. But it pays to not be complacent.

For the background on how China now publishes gold trade data see my LBMA Alchemist piece from earlier this year.

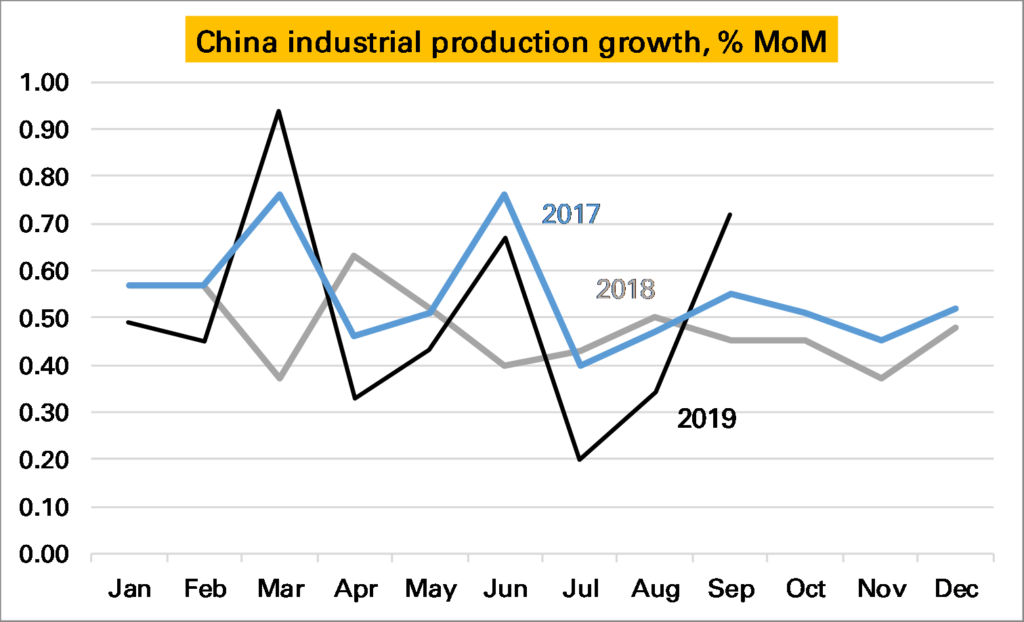

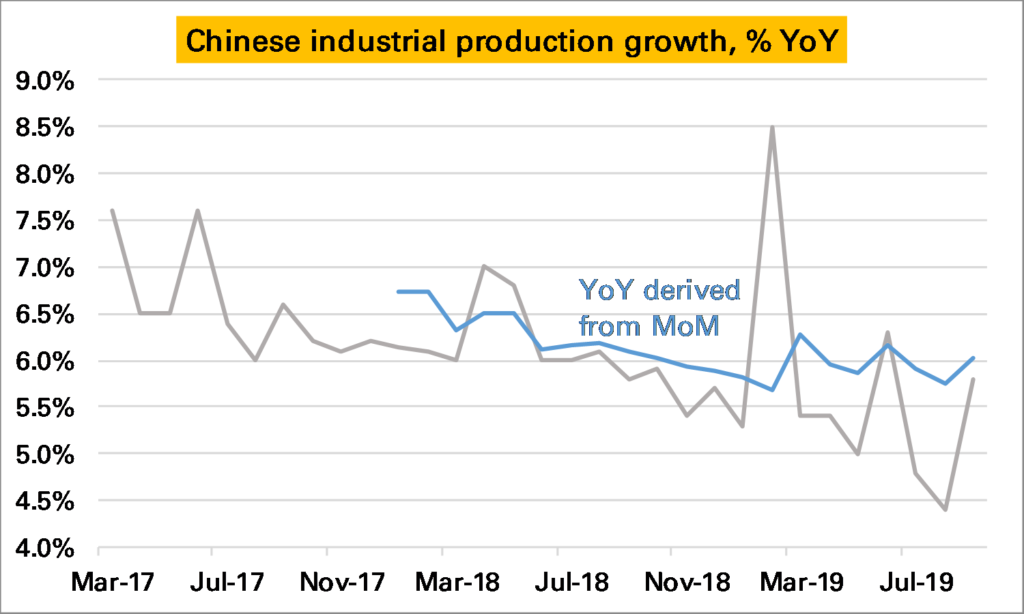

Last month I suggested that Chinese industry was not doing as badly as the August year-on-year (YoY) series suggested, a rise of just 4.4%. This was because the seasonally adjusted month-on-month (MoM) series, theoretically a much better guide, implied a higher YoY rate of 5.5%.

September’s data was released today and shows the YoY series rebounding more strongly than market expectations, now up 5.8% YoY.

In part this was because September saw a strong 0.72% MoM increase.

Source: NBS, Matthew Turner, October 2019

But it also looks like some catch-up with the implied YoY series.

Source: NBS, Matthew Turner, October 2019

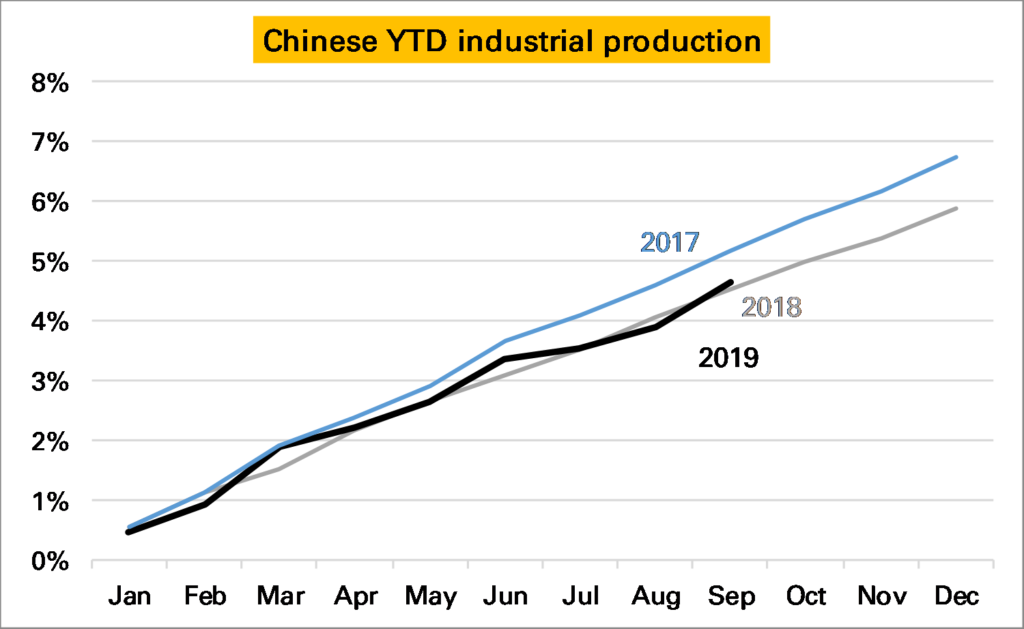

Year-to-date (YTD) Chinese industry is actually slightly outperforming how it did in 2018 using this MoM data*.

* Of course one might not believe any of the data series.

Answer: it wasn’t and that was a good reason to think the price of palladium could go higher. And indeed it has gone higher, now nearing $1,800/oz.

We now have North Macedonia trade data for August. Does this show any shift towards platinum? Nope. Palladium was 44% of the palladium & platinum imported, higher than the YTD average of 36%. This reinforces the point that 2019 is on course to see palladium’s share rise not fall.

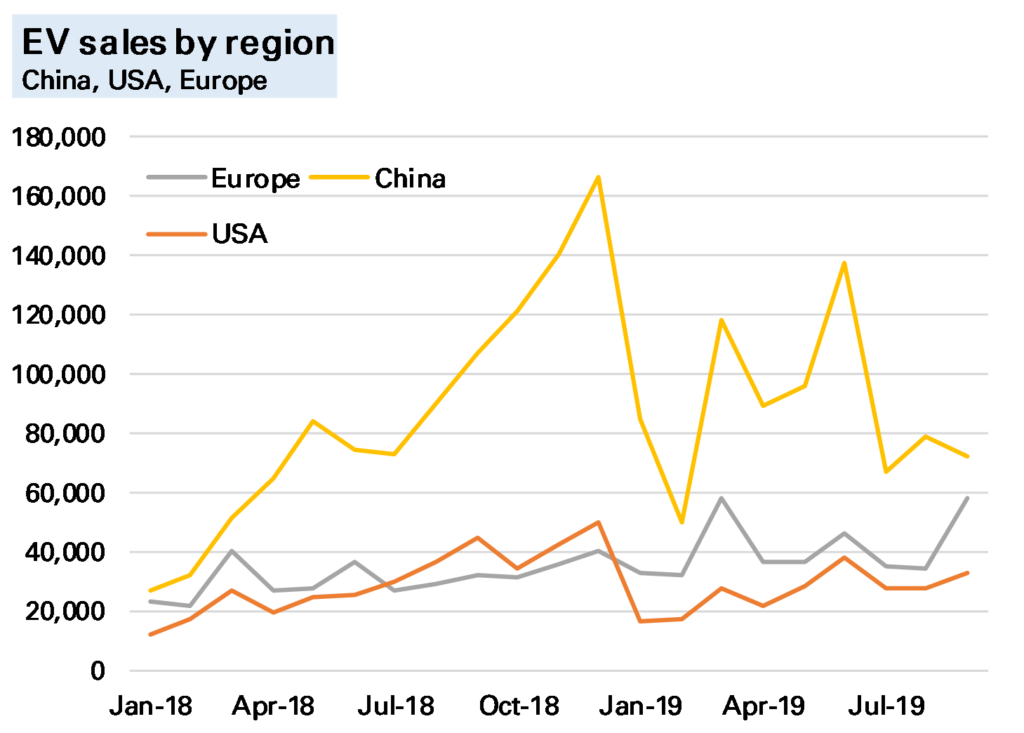

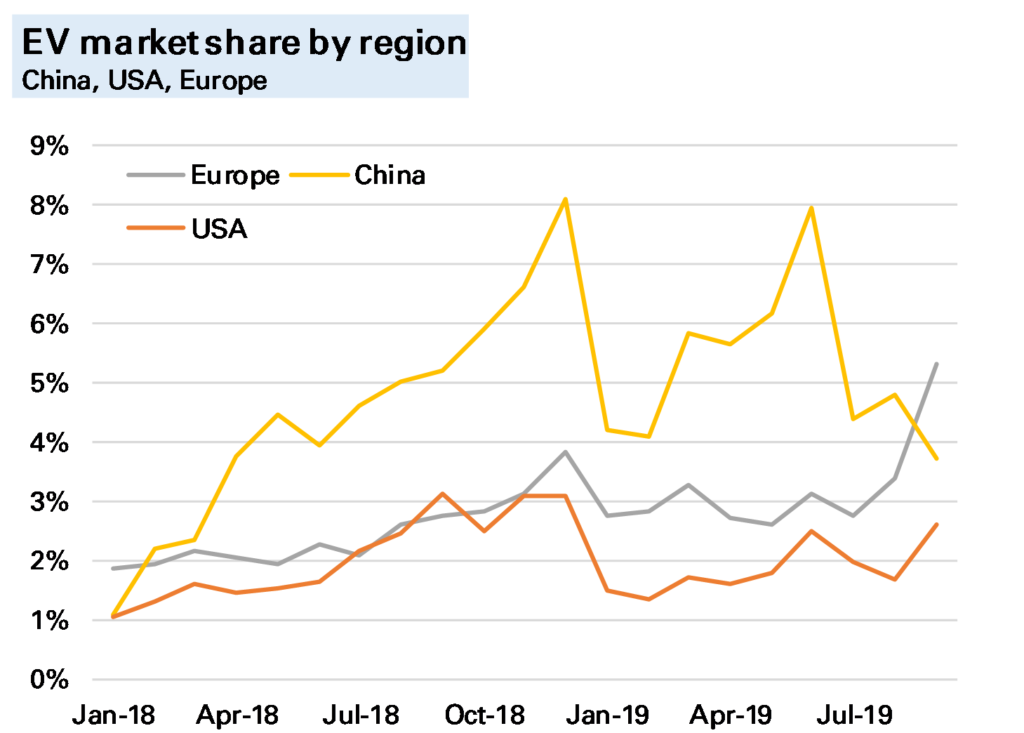

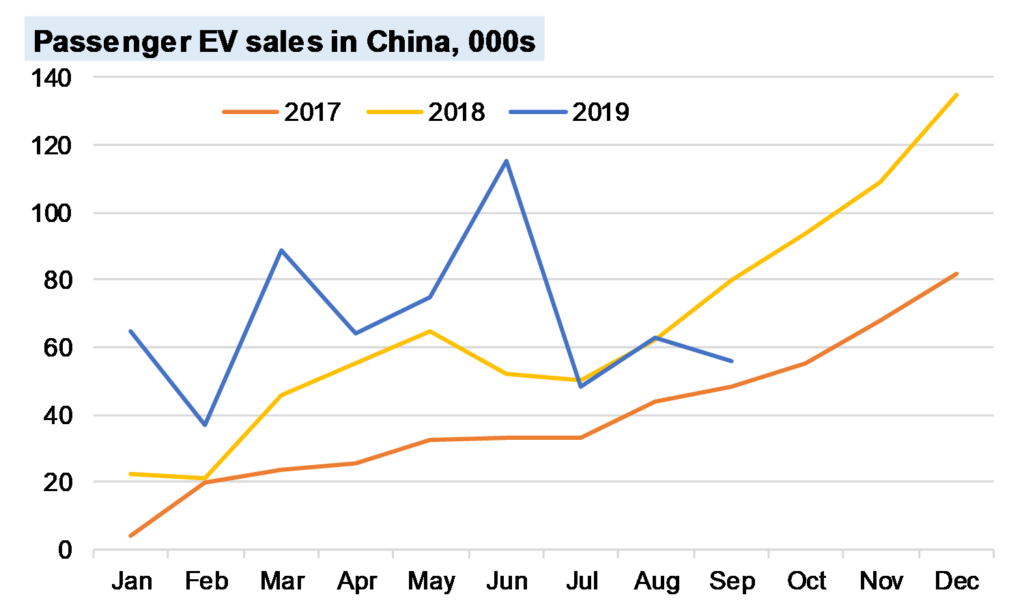

While global EV sales were disappointing in September, down 11% YoY, those in Europe continue to soar, gaining 82% YoY. And while Europe remains far behind China in EVs sold YTD, at 369k cars, to 792k, in September the two markets were much nearer, at 58k to 72k. In market share, Europe was even a little higher than China, though I wouldn’t want to make too much of this, given I exclude from the totals some smaller EV markets where by definition market share is low.

Will this continue? It’s unlikely. Europe’s EV sales are rising, helped by subsidies and new model launches, though September is likely to prove exceptional given a backlog of Model 3 orders. And Chinese sales should improve into year-end, if not at the same pace as in previous years.

Source: National car data, Insideevs.com, Matthew Turner, October 2019

In today’s latest World Economic Outlook (WEO) the IMF devotes a large-ish section to gold and other precious metals (p.47 onwards here).

Perhaps the most interesting section is on whether they serve as an inflation hedge. Finding a positive but weak correlation to inflation itself, the analysts also look at gold prices against modelled inflation risks. Here they are more positive, saying:

Results of the analysis support the view that precious metal prices react to inflation concerns… An increase in inflation uncertainty by one standard deviation tends, within a month, to raise the price of gold by 0.8 percent and silver by 1.6 percent. A decline in inflation uncertainty can explain half of the observed gold price decline of the 1990s and one-third of the price rise after 2008. The role of inflation uncertainty is, instead, positive but not significant for platinum and palladium, yet irrelevant for copper

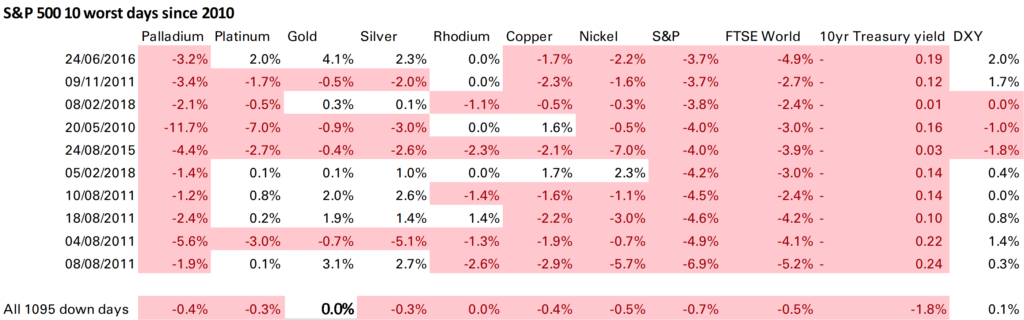

For many gold’s main advantage is not inflation but against systemic risk. The IMF also looks at this through reactions to S&P 500 moves. This is something I have long done, and the IMF’s conclusions are the same – gold does act as a safe haven when the S&P 500 falls, silver does but less so, and the other metals do not. Here’s one of my versions of this table.

Finally the IMF also mentions precious metals’ sensitivity to dollar moves. But only to express surprise the beta can sometimes be more than 1 (ie if the dollar falls 1%, gold rises more than 1%). I think this relationship – which is partly obvious given we are quoting the price in dollars – needs more discussion and will do so in a later post.

Globally 170,000 electric vehicles (EVs) were sold in September, 11% lower YoY, with pure EVs (BEVs) falling YoY for the first time. This I calculate using national data released in the last two weeks.

Regionally there was a very strong performance in Europe, where YoY sales were up 82% YoY (note revised from 75% in the linked article), boosted by pent-up sales of Tesla’s Model 3. However in the USA weakening sales of the Model 3 compared to its own, earlier, 2018 boost was a major factor in EV sales falling 26%.

But the biggest impact on the global numbers remains China, and there sales of EVs were very weak, down 34% YoY. With China accounting for around half of global EV sales in September 2018 (and still more than 40% in September 2019) this clearly dragged the global total down.

All Chinese car sales were down 6% YoY, but the slump in EV YoY is more due to reduced subsidies and perhaps some signs Chinese consumers are worrying about value for money, especially resale value. It’s also exacerbated by the strong start to the year and the exceptionally strong end-year performance seen in both 2018 and 2019, which seems missing this time around.

In commodity markets it seems widely accepted that market deficits are price bullish and market surpluses price bearish. Intuitively this feels right. A deficit is when demand is higher than supply and inventories (stocks) are falling. Such a situation cannot go on forever, as stocks are not infinite. Ultimately demand has to fall or supply has to rise, and in the absence of other factors (recession, technology etc) the way this happens is via a rising commodity price.

In practice it is not so clear cut, and the easier it is to hoard the commodity, the less clear cut it gets. For metals, and particularly precious metals, where hoarding is not only easy but often desirable, the picture is very muddy indeed.

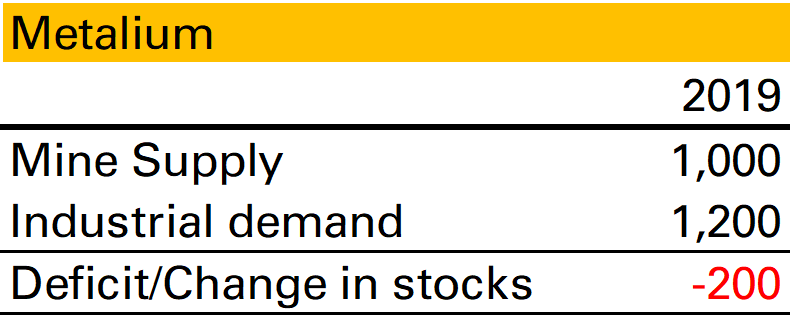

Take this S&D for Metalium, a made-up industrial metal. In 2019 1,000 units were supplied by mines, 1,200 were demanded by industry. This makes a deficit of 200, or put another way, a fall in stocks of 200. If I asked you what happened to the price in 2019 you would probably assume it moved higher.

Bullish? Bearish?

But what if I then told you that actually what happened was industrial users midway through 2019 saw that 2020 was set to be a very bad year for demand and decided to reduce their stocks by 200?

This now seems bearish! Most likely those 200 units flooded the market, pushed the price lower, boosting industrial demand and reduced mine supply.

In other words whether a deficit is bullish or bearish can depend on the reason stocks are falling.

In base metals, where stocks are mostly held within industry and are relatively stable, this latter scenario might not be that common. But in precious metals it happens all the time, as the stockholders are not industrialists but investors. If in an otherwise balanced market a very large investor decides the future of platinum is bleak and sells their holdings of 1 Moz, the market will be in a 1 Moz deficit but the platinum price will be a lot lower.

So on a static snapshot, market deficits are not necessarily bullish. But maybe we can at least say that they imply a higher future price? After all as we noted at the beginning of this piece, stocks are not infinite. A deficit might reflect a bearish investor throwing in the towel, but they can’t keep throwing in the towel. Ultimately there will come a point when there are no more stocks (or no-one wants to sell their stocks) and the commodity price will have to rise to bring supply and demand back in line.

This is more justifiable, though still not always true. Consider these two scenarios:

The industrialists or investors are right in their pessimism, and so a deficit in one year is followed by weaker demand or higher supply in the following year. In this scenario prices don’t have to adjust upwards.

The sale of stock is, in itself, new information that changes perceptions. An example would be if a European central bank announced, out of the blue, it had plans to sell gold.

Finally, for gold, where almost all demand is stockbuilding (by investors, but also by people in the form of jewellery) deficits and surpluses are even less well defined. I’ll have more to say about that in another post.

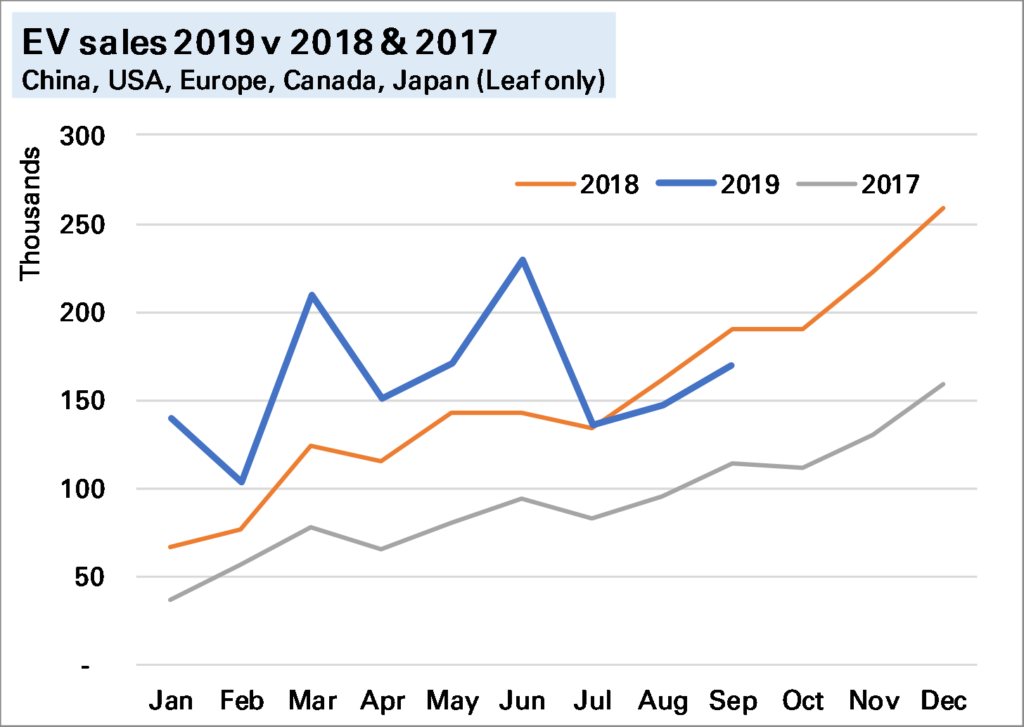

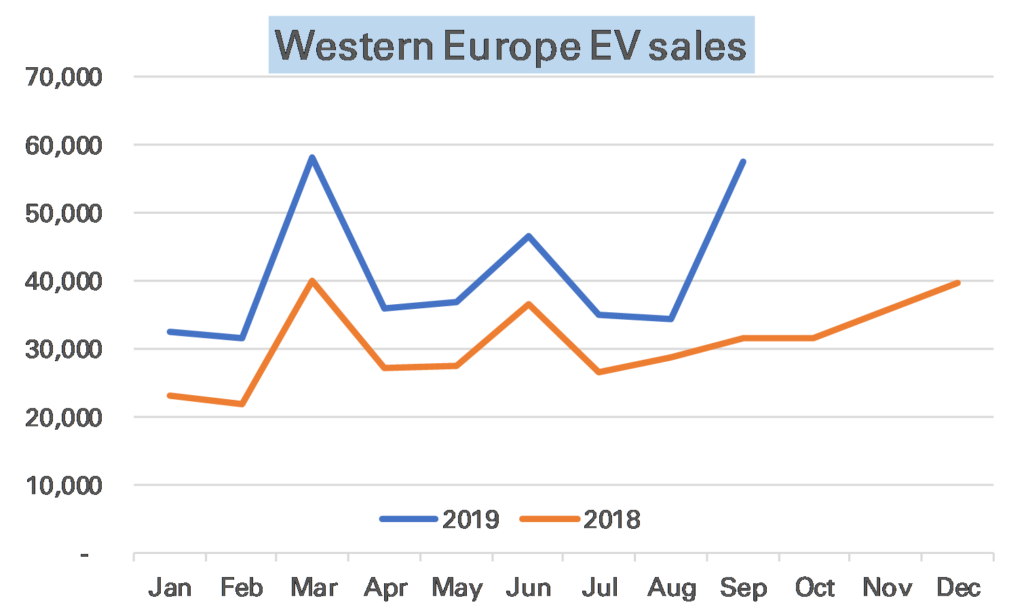

After a few months of a weakening trend, European electric vehicle (EV) sales in September roared (or maybe whined?) back, up a remarkable 75% YoY, led by a 112% gain in pure EVs (BEV) and with even plug-in hybrids (PHEVs) higher YoY.

I estimate total EV sales in the region were just under 58k, nearly matching the highest month in history, March 2019.

Source: European car association data, Matthew Turner, September 2019

What was behind this performance? That it was nearly a record month is partly sign of the market maturing. March & September are traditionally the strongest month for all new car sales in Europe, with number plate changes (particularly in the UK). It now looks like buyers are waiting for these number plates to get EVs too. The YoY acceleration is more interesting. Partly this was because it was a strong month anyway for all new car sales after a weak September 2018 on emissions changes – up 12% YoY on my estimates. Specifically, however, the roll out of Tesla’s Model 3 to Europe continues to have an outsized impact on EV’s market share.

The palladium price has hit a new record high in recent days over $1,700/oz, and the FT has declared there’s more to come unless we see a global recession or substitution of much cheaper platinum. I agree. And yet at present not only is there no evidence of substitution but there’s evidence that there has been no substitution.

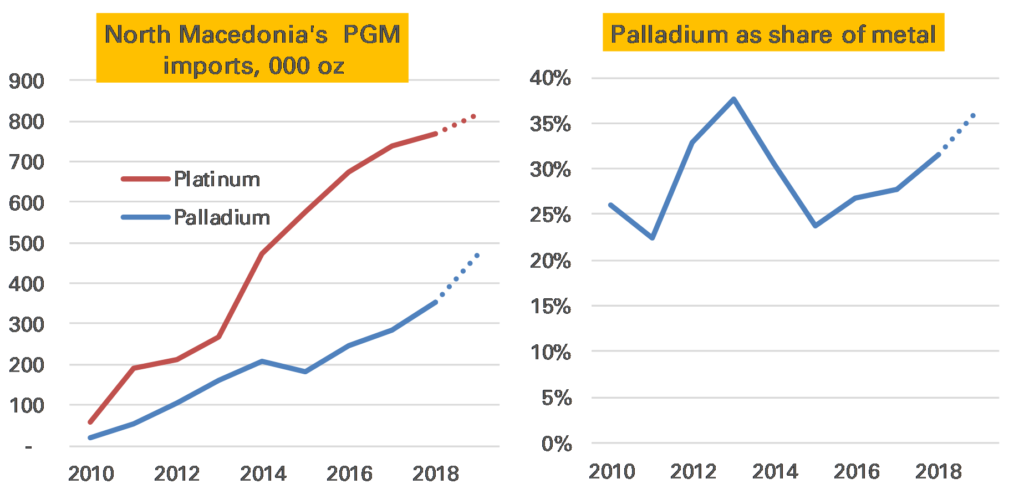

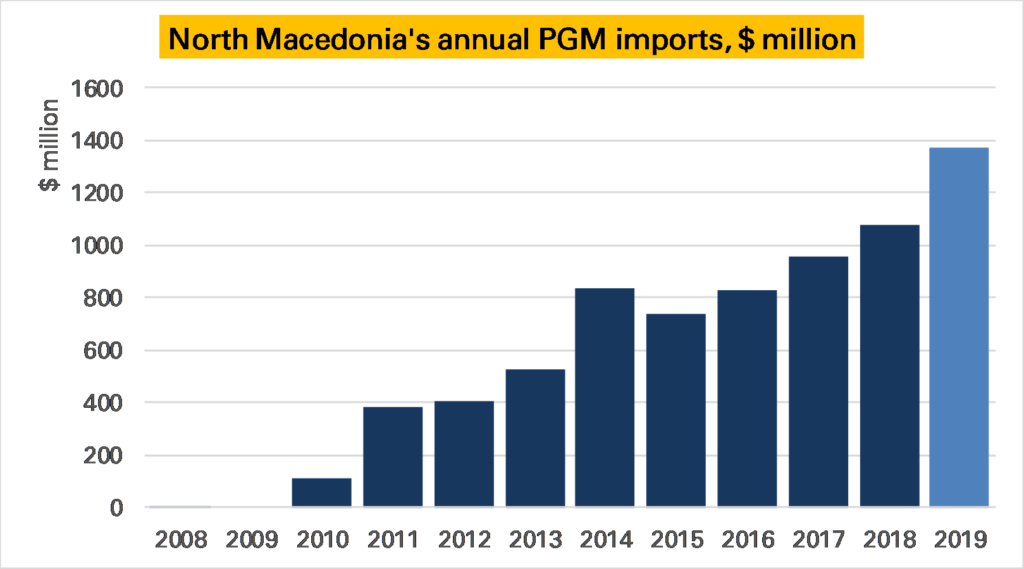

It comes from North Macedonia.

This country had little to do with the global PGM markets for much of its history. It is not a producer, and in 2009 reported imports of unwrought PGMs of only $1. That might sound a little implausible, but probably not far from correct – in 2008 PGM imports were less than $20,000.

And yet in 2010 it imported over $100m of PGMs. And by 2018 this was over $1bn, with more than 1 Moz of PGMs imported. This year is approaching $1.5bn.

Source: UN comtrade, Matthew Turner. Note 2019 extrapolated from first 7 months of the year.

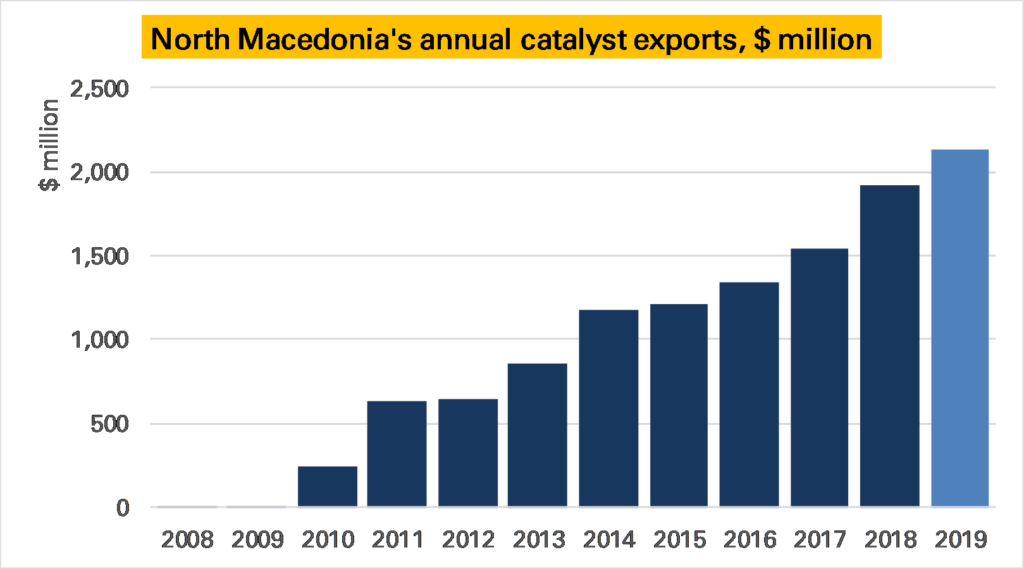

What gives? In 2010 refiner Johnson Matthey (JM) opened a diesel autocatalyst plant, which was expanded in 2013. This is why North Macedonia’s exports of catalysts also exploded, rising from nothing in 2008/2009 to nearly $2bn in 2018 (Macedonia has not gone its own car industry).

Source: UN comtrade, Matthew Turner. Note 2019 extrapolated from first 7 months of the year.

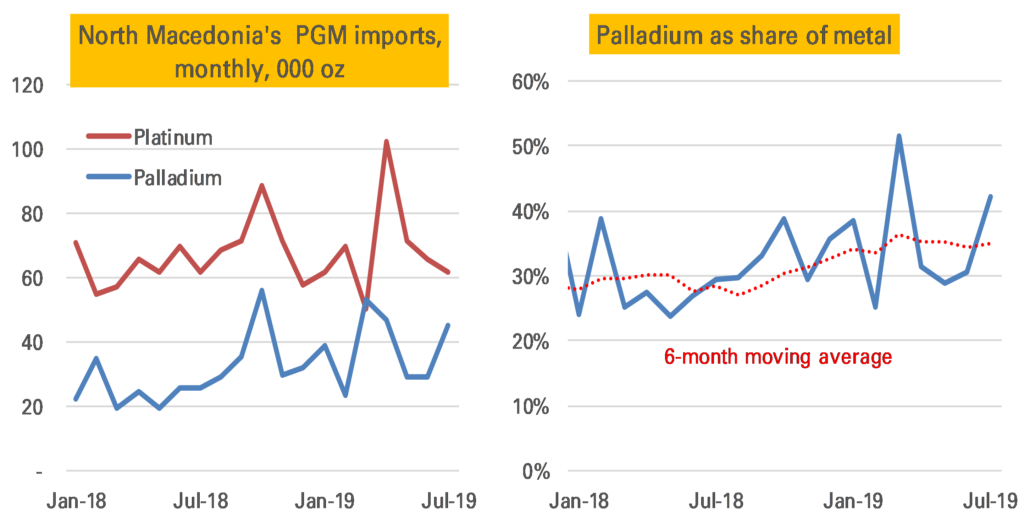

This is great for an analyst. Other large catalyst manufacturing countries are also PGM traders, such as the UK, and/or jewellery consumers, such as the China and the USA. This means it is hard to draw firm conclusions from trade data. But in North Macedonia it is just catalysts – therefore it is safe to assume the imported PGMs are being used in that sector.

As such because we can break the trade data out by metal we can use it to estimate what proportions of platinum and palladium JM are putting in their catalysts. If we look at its imports by volume, we see that more platinum is imported than palladium – in 2018 nearly 800 koz of the former to around 350 koz of the latter – making palladium 28% of the combined volume to platinum’s 72%. This is to be expected given the plant is producing diesel catalysts. But importantly this proportion of palladium in the mix doesn’t seem to have fallen in the last few years – indeed it modestly rose from 24% in 2015*.

Source: UN comtrade, Matthew Turner. Note 2019 extrapolated from first 8 months of the year. This chart was corrected on 23-10-2019 as date axis misaligned and so includes August data.

Perhaps the shift has only happened in the last few months? Not that either. Indeed while monthly import data is quite volatile, if there is a clear trend it is the other way, with palladium seeing a share of 50% in one month.

Note: The right-hand chart on 24-10-2019 replaced an earlier one which in error showed palladium relative to platinum, not as a share of all metal.

This data can’t prove no substitution is taking place. There could be other effects masking it, for example if JM have been importing additional palladium than they are using in catalysts (indeed it looks likely), perhaps ahead of the rising price or Brexit. It also might be that the mix of heavy and light vehicle autocatalyst could have changed, affecting the ratio (that’s what seems to have driven palladium’s share down in 2013 after the plant’s first expansion). And if the plant had begun manufacturing gasoline catalysts all bets would be off, though then we would also see rhodium imports, and we have not.

We also can’t assume that JM’s Macedonia plant is representative of all their catalyst plants or those of other catalyst manufacturers. And it is possible substitution is happening in gasoline catalysts, not diesel ones.

Nevertheless it is strong evidence that there has been no substitution. After all most analysts believe if substitution is to come it would come first in diesel, where car and catalyst makers are most comfortable with using platinum.